With financial institutions across America looking to add clients every day, community banks offer a distinct set of advantages they can leverage to win the new customer acquisition game.

To be successful, community banks must embrace what makes them different from their competition.

There are lots of great reasons for new clients to choose community banks, and I’m not just saying that because I work for them. To be successful, community banks must embrace what makes them different from their competition.

Sure, you’ve got an app, and you’ve got great products. So do they. Why not take the opportunity to focus on your bank’s successes in small business lending, or the fact that your clients can speak to real people who know them and their banking history—and that they can speak to that same person again the next time they call?

Even if you’ve already built a strong brand foundation, you must continue to attract, onboard, and nurture each new client, while making sure to remarket to those who haven’t made the switch to your bank. It’s the key to success, and something we have tons of experience doing for banks like yours.

1. Community bank clients prefer to support local, homegrown businesses.

Your bank’s deep-seated roots offer you a unique advantage over your larger, nationally focused competition. A shared passion for your community is attractive to clients and prospects alike.

Community banks are locally owned and managed—themselves small businesses within the community. Therefore, you’re likely aware of the same challenges that other local small business owners worry about.

With the continued rise of online and mobile banking, there’s a chance that the members of your community who prefer face-to-face interaction have just one brick-and-mortar banking option: your bank. In fact, one-fifth of all U.S. counties don’t have a single regional or national bank branch to serve the financial needs of their residents.

Right now, there’s a group of banking prospects who will always prefer personal contact—the ability to call a human being or come in to speak with one about their banking needs—over interactive voice response (IVR) systems. That’s a huge differentiator, and one you can offer to them using even the most basic marketing methods.

Too many times, we wind up trying to go toe-to-toe with a larger bank’s technology instead of simply communicating what truly differentiates us.

Don’t take for granted your ability to serve and market to local clients based on a shared passion for your region (or your tenure serving the needs of clients within it). Otherwise you could miss out on developing real, lasting relationships that strengthen both your bottom dollar and your community’s overall health and financial stability.

TAKEAWAY: Don’t forget to tell people that the experience at your bank is more human than the competition. Too many times, we wind up trying to go toe-to-toe with a larger bank’s technology instead of simply communicating what truly differentiates us.

2. Lending decisions go deeper than the numbers.

Community banks lend more than $3.5 billion to small businesses on an annual basis. Where larger banks might make decisions on predetermined formulas alone, you probably have more freedom to offer flexibility in lending, based on knowing more about each applicant—a cache of info that includes previous banking relationships, as well as character references and spending habits.

More than 50% of small business loans come from community banks.

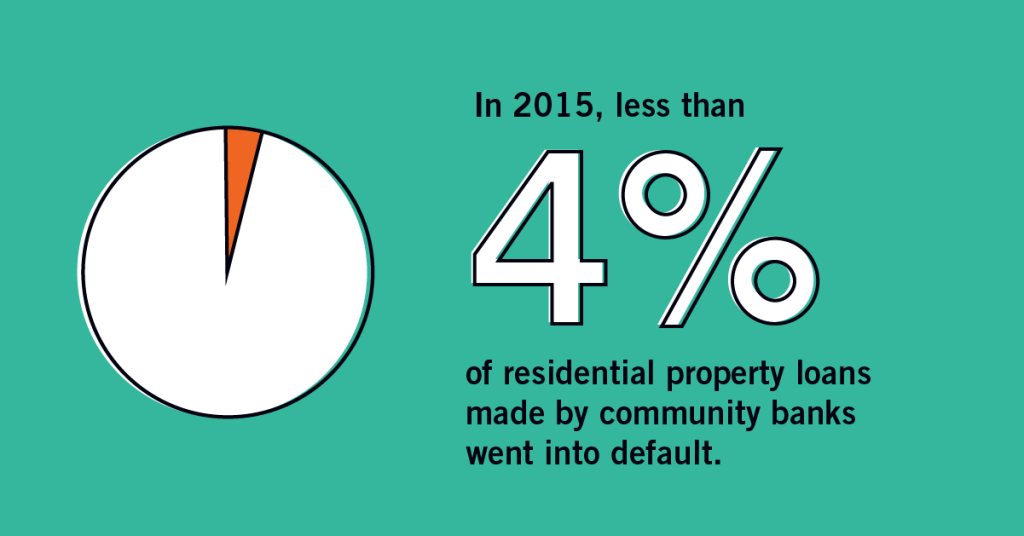

In 2015, less than 4% of residential property loans made by community banks went into default.

Local borrowers are more responsible with community bank loans versus those granted by larger, national banks. Less than 4% of residential property loans made by community banks went into default, compared to more than 10% for big banks, according to the same Harvard Kennedy School study.

Additionally, you’re able to provide ancillary benefits to small business owners. Most larger regional and national banks might approve or deny funding from nondescript locations far away. As a community bank, you have the opportunity to go above and beyond, approving loans with greater flexibility and helping your local clients connect with local suppliers, customers, and businesses.

TAKEAWAY: Base your lending decisions on the complete picture of each applicant, rather than strictly using formulas and calculations. This approach lets you offer ‘round-the-corner clients and prospects an experience that bigger, national banks are unwilling to provide.

3. Community bank clients are happier.

As a whole, the banking industry is getting better at customer service and satisfaction. But when it comes to getting the best, most personalized service, community banks are king. Regional and community banks recorded a 2018 ACSI satisfaction score of 84, with super-regionals (79) and national banks (77) lagging significantly behind.

Similar data is present on the business side of banking too, where community banks have become the small business lender of choice. According to the Federal Reserve’s 2019 Small Business Credit Survey, 79% of independent business owners who used community banks indicated satisfaction with their overall experience, compared with 67% for large banks and just 49% for online lenders.

Those solid relationships we talked about earlier? They’re built on satisfaction and trust. Take the story of Huff Ice Cream, a family-owned commercial business located in upstate New York.

During an annual review, Huff’s community bank loan officer encouraged them to consider adding flood insurance protection, even though the ice-cream distributorship had never flooded once during its 50-year history. Huff followed the banker’s advice and added coverage—which helped protect them from $1M in future losses when the business flooded twice in six years.

Clients choose community banks for the same reasons they choose the friends they spend time with—they know them, they trust them, and the banks have their clients’ backs.

TAKEAWAY: Community banks make people happy and garner more trust. Clients conduct more business with the banks they trust. This is low-hanging fruit: engage with your clients, and they’re more likely to stick around longer, use more of your products, and, most importantly, send you new clients who will boost your new deposit numbers—and help you sleep better.

Clients choose community banks for the same reasons they choose the friends they spend time with—they know them, they trust them, and the banks have their clients’ backs. With new client acquisition at the top of every bank CEO’s priority list, make sure to use the advantages you have as a community bank to your advantage. Whereas national lenders may come and go, your community wouldn’t be what it is without you there.

Strive to make lending and customer service decisions that benefit you, your clients, and your community—even if they require a little more time and effort—because they’ll pay off in the long run.