When someone buys a brand-new car, what do they say?

“Well, mine was getting up in miles. The trade-in value was dropping, and I really wanted something with better gas mileage.”

This is the rationale.

“I wanted something with more safety features.”

“I needed more reliability.”

“Have you seen the trade-in deals lately? They almost paid me to get a new car.”

These are the logical facts we share so we don’t look like an insane person for committing funds to a quickly-depreciating asset.

So what was the reason?

If we’re honest with ourselves, here’s how we’d really answer: “I saw an ad on Facebook during my pre-bed-time doomscrolling. The ad made me feel better than all the disquiet I’ve been feeling, so I clicked through. Building out a car online, to my exact specs, made me feel even better. If a virtual shopping experience feels this good, I imagine a test drive will make me feel ecstatic!”

Once, I asked an “expert” used-car salesman why all used-car ads relied on insane gimmicks with a pitchman yelling at the camera. Almost all consumers say they hate this style of advertising, yet it keeps going, and people keep buying cars.

His response: “You have to realize that for about 72 hours around the purchase of a car, the buyer could be considered legally insane. They’re making completely emotional decisions. These ads play into this emotion. And they work.”

Emotional buying isn’t limited to cars or even large purchases.

Do you really think you buy M&Ms because they “melt in your mouth, not in your hand?” No. You’re probably not even hungry when you buy them. They’re not healthy. They won’t sustain you very long. There are few logical reasons to buy junk food. You could buy a whole bag of salad for the price of a small amount of M&Ms. We don’t buy junk food for any rational reason. We buy M&Ms because they make us feel better, even in a small way.

People make decisions based on emotion, and they backfill with logic.

My mentor, Duane Birch, repeated this axiom to me almost every day we worked together. He never told me who told him first—or if he picked it up in his multi-decade national brand experience. From Yugo to Yoo-Hoo, consumers proved to lean toward what they want before they make certain it’s what they need. This Harvard professor agrees.

Ok. ok. But what about banking?

As a general rule of thumb, bank advertising relies on rationale—the secondary side of decision making. This is based on features, logic, and math. Banks (generally) don’t seem to realize people make decisions on excitement—impulse—how the brand makes them feel (if the brand is good).

Perhaps banks drank the wrong Kool-Aid and believed potential customers couldn’t be excited about banks. Maybe they forgot banks, almost literally, perform magic—transferring funds from your strong brick building to a trendy retailer to complete a purchase—almost at the speed of light.

Either we forgot how magical—how helpful—banking is. Or, at the very least, took it for granted and forgot to tell people.

Banking is emotional.

Most customers who switch banks do so for two reasons: poor service or a mistake (which likely wasn’t handled well). The customer is angry—they feel mistreated or unimportant. They feel emotional. And they want to find another bank that will not do this to them. They want a bank that will not make themfeel this way.

First, you must realize you’re not creating ads trying to convince satisfied people to leave their bank. As we covered in a past blog, only 2% of people are either Dissatisfied or Very Dissatisfied with their primary bank. You have a small potential audience who is ready to leave at any time. You must be ready with advertising messages created to speak to those looking to leave their current bank.

Second, you must build your message around a beneficial brand. To do so, you need to deeply understand the difference between benefits and features (and those features trying to be benefits). We cover that here.

Third, you must combine these into a consistent, benefit-based brand message. This is much easier said than done, but if it was easy to do, everyone would be doing it. Your advantage? Out of 5,000 banks, almost no one is doing this well.

How does that make you feel?

A paradox is an unanswerable question. One famous example is: “What happens when an unstoppable force meets an immovable object?” This question dates back to ancient China and is credited with creating the word “contradiction” in the Chinese language. The adjectives do the heavy lifting here. If something is truly unstoppable, an immovable object can’t stop it, and the force can’t move it.

So, what gives? Nothing. Except maybe our minds—which tend to explode over problems like this.

Banking also has a conundrum.

As part of its Unconventional Convention, the American Bankers Association unveiled a research report by Morning Consult that outlined customer sentiment in banking. This study showed a statistically overwhelming positive sentiment for community banks.

89% of those surveyed indicated they were satisfied or very satisfied with their primary bank.

96% said their primary bank’s customer service could be characterized as good, very good, or excellent.

That’s a helluva good job! These are awesome stats, and we celebrate with you. The survey goes on to outline even more positivity, specifically around banks’ response COVID-19.

But as we look forward to a day beyond the pandemic, where we fall back into our norms of loans and deposits, this survey provides a bit more information.

Unstoppable Goals. Immovable Customers.

When you look at the data one way, it shows your customers are likely satisfied (or better). This is good news for you. And bad news for every other bank.

But what happens when you’re the other bank? Most banks are flush with deposits due to PPP funds being held, but those dollars will flow out eventually. The world will return to normal (new or not), and we’ll face our old goals.

We learn from the same survey that only 1% of bank clients are very dissatisfied with their primary bank. Another 1% are simply dissatisfied. Generally speaking, customers have to be on the more extreme side of this scale to leave.

New deposits? New loans? Those come from new customers—and we’re faced with asking someone to leave their primary bank where only two out of every hundred customers are looking to leave their bank at any given time.

This is the paradox. Your bank must continue to grow. But customers aren’t looking to leave.

Loosing the Gordian Knot

Some paradoxes do have answers, but you generally have to cheat—or at least think laterally— to find a solution. Another well-known paradox is the Gordian Knot. If you want the full story, I recommend the Wikipedia entry.

The short version is thus: Alexander the Great was confronted with a prophecy: an oxcart was hitched to a post with the Gordian Knot—one so complex it could not be untied. It was foretold that whoever unraveled this knot and unhitched the cart would be the ruler of all of Asia (then defined as basically the Middle-East).

Although Alexander was great, he first approached the problem as most of us would: when confronted with a knot, one tries to untie it. The problem was the knot was so tangled and intricate that it was truly impossible to untie. We do it all the time. We confront a problem based on preconceived notions. This is the underlying reason why almost all magic shows are entertaining, and most jokes are funny. The payoffs of both subvert our expectations to humorous or astonishing effect.

There’s another saying: “when you’re a hammer, the world is a nail.” We try to find solutions with the criteria at hand.

There are two versions of Alexander’s solution.

The more straightforward version rumors he cut the rope. Another version (for all the purists) says Alexander pulled the lynchpin of the wagon’s yoke, pulled it through the knot (thus unraveling it), rehitched the yoke, and dusted his hands in satisfaction.

It turns out even paradoxes are paradoxes. What is supposed to be unanswerable can be answered. This is even true of unstoppable forces and immovable objects.

Stopping the Unstoppable

You might say, “But Alexander found a loophole and exploited it!” To that, I say, “yes!” Solutions to complex issues can be found more in looking for answers than the problem itself. What didn’t the rules say?

The place to start on our banking quandary is to stop—stop the 1-2% fromleaving your bank.

When researching for this article, a startling trend became apparent: folks aren’t thinking about retention. There is a dearth of research on what makes customers leave. There is plenty of data on what they say when they leave, how likely they are to say it, how to re-attract them, the costs associated with customer loss, BUT very little available research on WHY.

The clearest assertation comes from Michael Leboeuf’s book, How to Win Customers and Keep Them for Life (2000). Laboef breaks it down as follows:

1% die

3% move away

68% quit because of an attitude of indifference towards the customer by the staff

14 % are dissatisfied with the product.

9% leave because of competitive reasons.

Unless you have a warlock on staff, we can skip addressing “death.” If these general business numbers hold true for banking, the first answer is simple: train your people well. I’m sure when you agree in assuming it’s likely that dissatisfaction in community banking leans more toward product and competitive reasons.

“We have all the products of a big bank” is a truth, but many of those megabanks outpace the off-the-shelf options given to us by our limited vendors. While there is little you can do about this, you must be willing to push vendors and upgrade when possible. The world waits for no bank.

“Competitive reasons” for banks can probably be expressed as a word: rates. You won’t win every deal. You don’t have to be told this, and there’s not much you can do here. You can determine exactly what’s going on in your bank by performing your own satisfaction survey. It’s a great way to reconnect with clients, hear their needs, and rekindle communication.

We’re only talking about protecting 1-2% who aren’t satisfied, though. Once we have the trickle plugged, it’s time to move onto the more daunting task.

Moving the Immovable

The answer to the first paradox is astoundingly (and perhaps frustratingly simple). What happens when an unstoppable force meets an immovable object? The force goes around the object. The framework of the problem urges you to solve the problem directly, but more often than not, it’s simpler to sidestep the issue with lateral thinking.

Banks ensnare themselves in this trap almost every time they sit down to create an ad. Look at the field of banking ads. Yes. They’re all the same. And almost all fail to live up to their potential for one key reason: they’re made to convince someone (anyone) your bank is good.

They’re written, designed, filmed, and published to simply inform about your bank. This happens under the guise of “branding.” We have to inform people about our brand!

Sure.

But now it’s time to upgrade those efforts.

It’s time to consider the 1%.

Before we go any further, let’s back up and look at the numbers. 89% of bank customers are satisfied or very satisfied. Yes, an overwhelming majority, but stop for a second and consider how you’d react if one of every ten customers who interacted with your bank was not satisfied or very satisfied?

One more aside. It’s easy to get too focused on the paradox and say, “Well, if I lose 1% and my competitor loses 1%, we’re just trading customers.” Keep in mind you might have to guard your 1% against ten competitors, but you have the opportunity to grab 1% from eachof those ten competitors.

So how do you upgrade your bank ads to win this battle? You create ads for the 1% actually in play—those looking for a new bank. Stop making generic ads stating the obvious to everyone in your town. Think about the person who’s making the drastic decision to leave his/her bank. Would you speak differently to a person you knew was about to make a banking change than one who didn’t give you that information? I hope the answer is “yes.”

While this audience hasn’t raised their collective hands, they’re out there. They’re ready to move. Turn your advertising toward them.

Instead of saying: “We provide really good service!” (like every other bank), say: “Make the move to the banking service you’ve been missing.”

Replace “11 convenient locations” with “Looking for a bank closer to home?” What if they don’t live close to your bank? The message won’t resonate with them. But you know whose bell it will ring? Bingo. Those who live close.

And, yes, target these messages whenever possible. But these are meant as stark examples to confront the innate fear of using a message that might not resonate with everyone in your markets. Would you rather move 100% of your audience 1% or 1% of your audience 100%?

Not convinced? Our methods and philosophies probably don’t resonate with you. It’s ok. You’re part of the immovable 99%. For everyone else, we’ve said enough.

Listen to our bonus discussion with Josh Mabus, Kevin Tate, and Robbie Richardson below.

Community bankers face one of the harshest competitive environments in any industry. At times it can feel we’re adrift on a sea of sameness—in undersized vessels—while gigantic megabanks churn the waters around us.

It’s difficult. We struggle to differentiate ourselves from similarly-sized competitors while contrasting our value against larger banks.

But there’s an alarming trend that I’ve seen emerge from this. Community banks tend to be very insular and cagey against the competition. This is fine—excepting one thing: too many community bankers have never darkened the door of the competition. This leads to making uninformed claims about our own products and service.

We’re the friendliest bank.

Our service is the best.

We’re much more efficient.

But. Do you really know that?

As with anyone thrown on the waves of choppy water, it’s no wonder we cling to what feels safe.

Have you ever opened an account at a competing bank? Have you ever tried their products or services to make an unbiased comparison against yours?

I’m worried that too many of us will say “no.”

Now, this isn’t some kumbaya guide to getting along. Quite the opposite, actually.

You can look at it two ways:

A vital part of warfare is scouting the enemy.

How can you ethically compare yourself to the competition if you’ve never experienced what they have to offer?

You can pick either because both are true.

Perhaps you say, “We don’t cast ourselves against the competition. We do our own thing—our best every day.” That is a valid and admirable approach. But, again, it’s insular.

You’re discounting the options from which a potential client must choose. I am not suggesting you advertise “Our bank is better than XYZ Bank.” You don’t have to (and shouldn’t) name the competition. But you can rest assured that clients will consider more than one bank when choosing their primary financial institution. It is your job to understand what your bank does better and make very certain a potential client knows.

I suggest that you can enhance how you serve clients and your community by understanding the offerings present in your bank’s footprint. Otherwise, how do you know what is missing from your bank’s offerings? From your client’s experience? What could you offer that no other bank brings to bear? These could be concrete concepts like products or abstract offerings like service and availability.

Perhaps it’s even simpler.

One day, a bank that serves small businesses will realize that the bank is only open during the entrepreneur’s busiest hours. That bank will shift its hours to 10am – 7pm to be available for that client base and will win business.

We tend to internalize that the grass is always browner on the competitor’s side. This is born from a sort of group egocentrism that “we” (wherever “we” might be) is best. Do you remember early in elementary school when you found out that the United States wasn’t the biggest country? Nor the most populous? There was no reason to have this belief. No one had told us that the US was larger.

We do not need to fall into a similar trap with our banks.

What if you find out the competition is actually super friendly? Or incredibly organized and efficient in processing loans? It probably makes you a bit sick at your stomach to consider that the competition is better in an area or two. Perhaps you find out that you kick THEIR tail.

Regardless, if you haven’t shopped the competition, you don’t know. And that’s dangerous.

I believe in this so much, I took $1,000 of my own money and handed it to Mabus Agency copywriter Riley Manning when he was relatively new to bank marketing. I told him to open 10 bank accounts at 10 banks. It was one of the best training exercises for Riley as he learned about banking. But it was also eye-opening as we engaged with several types of banks. We were constantly surprised about which one was really good (or really bad) in certain aspects of banking.

As you prepare to shop the banks with which you compete, I suggest you watch and listen to Riley as he recounts his adventures—and dig deeper into our special blogs that capture, in detail, what he discovered.

Learn from Riley’s direct experience, but also use our rubric in your approach and valuation of the competition. It’s worth the effort. And your grass will be greener because of it.

Consumers don’t think about banking.

As bold as that statement might be, it probably doesn’t really rattle your cage. Now think about how you talk about your clients with your peers—within the bank.

“Earn up to half a basis point more on our demand deposit product by meeting four of our seven simple qualifying criteria.”

But consumers don’t think about banking. Bankers think about banking.

Now that doesn’t mean that consumers’ minds aren’t on financial topics. They just don’t think about it like you and I do. They’ve never studied the Truth in Lending Act and certainly don’t know the difference between an investment advisor and a fiduciary—or even that interest is cool because it compounds.

Consumers think about…

Making ends meet.

Can I afford a new house for when the baby comes?

Am I going to be able to retire?

How do I save more money?

Or even more simply:

How do I take care of my family?

Can I avoid being a financial screwup?

Most of us meet those questions with bank speak: “Earn 1.23% APY With a Flexible Savings Account.”

Or even worse, a robot impersonating a human: “I Can Bank While I Wait in Line at the Food Truck.”

Yes, those are real examples, and not just special cases. We see a lot of similar ads.

In the financial industry, we think about banking. In the real world, people just think about money.

For most Americans, their bank is just where their money is deposited. A vast majority (82 percent) of US workers have their paychecks direct deposited*—pretty impressive adoption seeing as how almost 7 percent of households don’t even have bank accounts. Their money goes into an account, they check the balance online, and they use a debit card to spend the money.

Other than a random fee, promotional email, or account hiccup, most Americans don’t think about their bank or banking at all. And there is no more brand loyalty associated with banks (the institutions most Americans trust with their entire net worth) than any other retail category. In fact, eight in 10 millennials would switch banks for better rewards.** Sure, millennials have lower brand loyalty than other generations, but not by much.

But they worry about money a lot. We’ve all heard the stats:

One reason people don’t think about banking is because they don’t understand it. I have a brain, and I’m very invested in the health of my brain, but I don’t think about neuroscience too often, because I just don’t understand it.

Your clients don’t understand finances, but they do have to use them every day. That’s incredibly frustrating, and leads to an incredibly striking stat: more than half of Americans have cried about money.

Why?

Maybe it’s because I could rock the Pythagorean theorem by 9th grade but didn’t know how to use a check register until I was in my 20s. Was it the school’s fault? Maybe. My parents? They tried—trust me. Some of my friends’ parents never mentioned money, though—because they didn’t understand it either.

But there’s a difference between fault and responsibility.

Maybe it’s no one’s fault—and by that logic, everyone’s fault. But let’s not assign blame. Let’s talk about responsibility and, even more than that, opportunity.

Your bank can take responsibility for your clients’ financial fitness, and in return, you can reap the rewards of having more financially literate clients.

I don’t think bankers intentionally do a poor job of explaining banking to their clients.

I suspect it’s much more innocuous than that.

Our minds are on banking—so much—all day, we simply forget that the consumer doesn’t think about money in our terms.

Bankers, like everyone in business, think, “I know my customers because they’re like me.” But that’s just not true, because you are a banker and your clients aren’t bankers.

My boss will often compare it to hunting ducks. When you hunt ducks, you probably quack like a duck and put decoys out to look like a duck, but your role is not to be a duck. You may understand ducks very well, but the moment you become a duck, the very nature of the transaction changes.

You have to remember that you are not the client. The client is not you. You’re there to serve the client—and it’s better for everyone when you serve on the clients’ terms.

And your clients and prospective clients need to know how banking works. Or you at least have to translate banking enough so the client can understand his/her role. And if you can tell them, you will forever be the easy and approachable bank in their mind. And the earlier you start, the more your bank will benefit.

Imagine this scenario. You explain the basics of automatic savings products, the way compounding interest works in your IRA accounts, and the benefits of having a checking account with FDIC insurance to a recent high school graduate who is about to start a summer job before going off to college. If that student takes any of your teachings to heart, they’re going to graduate from college with a little money and a good idea of how to stretch their new big-boy salary a little further.

That client is likely going to meet someone, fall in love, get a promotion, get married, buy a house, have some kids, buy a bigger house, open a college savings account, take out a HELOC, double down on retirement, open a trust account, and the list goes on.

Where do you think they’re going to open those accounts? At the bank that taught them how money works—the bank that related to them on their terms.

That is, if they know how banking and money work. Otherwise, they’ll open a checking account, leave a few hundred dollars in it each month, live paycheck to paycheck, and never really learn how to grow their wealth.

Most bank products were created to meet a client’s needs. But bankers accidentally explain those products with bankerly jargon. So opening their eyes to the possibilities offered by a wider range of financial products brings your clients value—if you can connect on the clients’ terms. It empowers your client while increasing your bank’s share of wallet.

(Side note: FDIC is a real big “duh” for us bankers, but most bank clients have no idea what it means—no matter how many tiny logos we put on ads or obscure plaques are displayed in our lobbies. Tide has been reminding Americans for more than half a decade that “Tide cleans clothes.” Duh, it’s clothing detergent. But they’re beating their competition. Be the only bank in America that truly reminds clients that their money is insured. Who cares if your competitors think it’s silly?)

Community banks are here to help the community. Let’s help them—first by helping them understand.

So you’re asking, “But, JB, it’s so complex—where do we even start?”

Well, the foremost experts in banking in your community are at your bank. Start with your clients. They’ll be so happy they’ll tell their friends. So then explain banking to your clients’ friends. After that, go to the young families in your community (they’re probably applying for homes with your mortgage department). Visit the schools (there are plenty of financial literacy packages to sponsor and/or use outright). Write about it on your website—nothing too fancy.

Tell them how banking works. Help them protect their finances and plan to grow their wealth. They’ll remember you for it.

With financial institutions across America looking to add clients every day, community banks offer a distinct set of advantages they can leverage to win the new customer acquisition game.

To be successful, community banks must embrace what makes them different from their competition.

There are lots of great reasons for new clients to choose community banks, and I’m not just saying that because I work for them. To be successful, community banks must embrace what makes them different from their competition.

Sure, you’ve got an app, and you’ve got great products. So do they. Why not take the opportunity to focus on your bank’s successes in small business lending, or the fact that your clients can speak to real people who know them and their banking history—and that they can speak to that same person again the next time they call?

Even if you’ve already built a strong brand foundation, you must continue to attract, onboard, and nurture each new client, while making sure to remarket to those who haven’t made the switch to your bank. It’s the key to success, and something we have tons of experience doing for banks like yours.

1. Community bank clients prefer to support local, homegrown businesses.

Your bank’s deep-seated roots offer you a unique advantage over your larger, nationally focused competition. A shared passion for your community is attractive to clients and prospects alike.

Community banks are locally owned and managed—themselves small businesses within the community. Therefore, you’re likely aware of the same challenges that other local small business owners worry about.

With the continued rise of online and mobile banking, there’s a chance that the members of your community who prefer face-to-face interaction have just one brick-and-mortar banking option: your bank. In fact, one-fifth of all U.S. counties don’t have a single regional or national bank branch to serve the financial needs of their residents.

Right now, there’s a group of banking prospects who will always prefer personal contact—the ability to call a human being or come in to speak with one about their banking needs—over interactive voice response (IVR) systems. That’s a huge differentiator, and one you can offer to them using even the most basic marketing methods.

Too many times, we wind up trying to go toe-to-toe with a larger bank’s technology instead of simply communicating what truly differentiates us.

Don’t take for granted your ability to serve and market to local clients based on a shared passion for your region (or your tenure serving the needs of clients within it). Otherwise you could miss out on developing real, lasting relationships that strengthen both your bottom dollar and your community’s overall health and financial stability.

TAKEAWAY: Don’t forget to tell people that the experience at your bank is more human than the competition. Too many times, we wind up trying to go toe-to-toe with a larger bank’s technology instead of simply communicating what truly differentiates us.

2. Lending decisions go deeper than the numbers.

Community banks lend more than $3.5 billion to small businesses on an annual basis. Where larger banks might make decisions on predetermined formulas alone, you probably have more freedom to offer flexibility in lending, based on knowing more about each applicant—a cache of info that includes previous banking relationships, as well as character references and spending habits.

More than 50% of small business loans come from community banks.

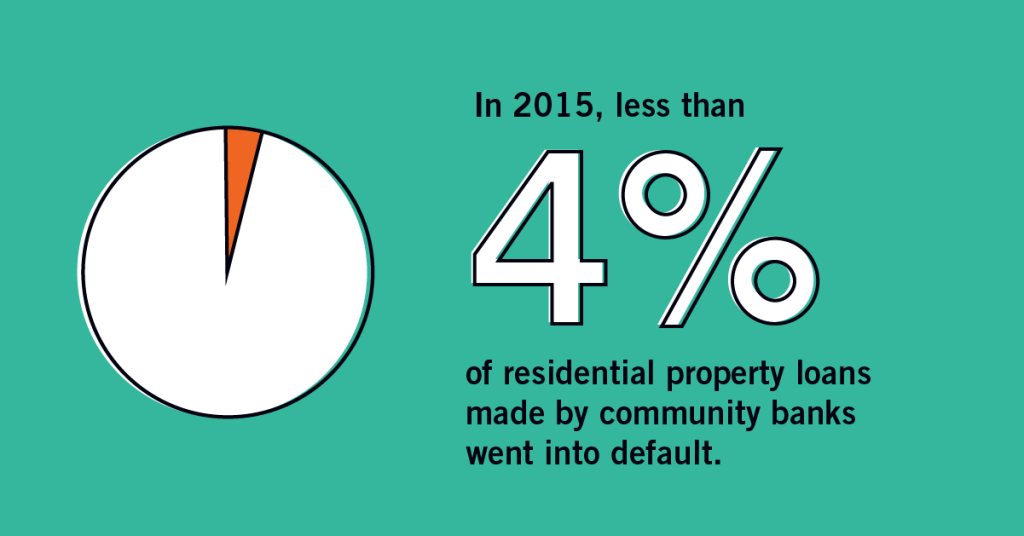

In 2015, less than 4% of residential property loans made by community banks went into default.

Local borrowers are more responsible with community bank loans versus those granted by larger, national banks. Less than 4% of residential property loans made by community banks went into default, compared to more than 10% for big banks, according to the same Harvard Kennedy School study.

Additionally, you’re able to provide ancillary benefits to small business owners. Most larger regional and national banks might approve or deny funding from nondescript locations far away. As a community bank, you have the opportunity to go above and beyond, approving loans with greater flexibility and helping your local clients connect with local suppliers, customers, and businesses.

TAKEAWAY: Base your lending decisions on the complete picture of each applicant, rather than strictly using formulas and calculations. This approach lets you offer ‘round-the-corner clients and prospects an experience that bigger, national banks are unwilling to provide.

3. Community bank clients are happier.

As a whole, the banking industry is getting better at customer service and satisfaction. But when it comes to getting the best, most personalized service, community banks are king. Regional and community banks recorded a 2018 ACSI satisfaction score of 84, with super-regionals (79) and national banks (77) lagging significantly behind.

Similar data is present on the business side of banking too, where community banks have become the small business lender of choice. According to the Federal Reserve’s 2019 Small Business Credit Survey, 79% of independent business owners who used community banks indicated satisfaction with their overall experience, compared with 67% for large banks and just 49% for online lenders.

Those solid relationships we talked about earlier? They’re built on satisfaction and trust. Take the story of Huff Ice Cream, a family-owned commercial business located in upstate New York.

During an annual review, Huff’s community bank loan officer encouraged them to consider adding flood insurance protection, even though the ice-cream distributorship had never flooded once during its 50-year history. Huff followed the banker’s advice and added coverage—which helped protect them from $1M in future losses when the business flooded twice in six years.

Clients choose community banks for the same reasons they choose the friends they spend time with—they know them, they trust them, and the banks have their clients’ backs.

TAKEAWAY: Community banks make people happy and garner more trust. Clients conduct more business with the banks they trust. This is low-hanging fruit: engage with your clients, and they’re more likely to stick around longer, use more of your products, and, most importantly, send you new clients who will boost your new deposit numbers—and help you sleep better.

Clients choose community banks for the same reasons they choose the friends they spend time with—they know them, they trust them, and the banks have their clients’ backs. With new client acquisition at the top of every bank CEO’s priority list, make sure to use the advantages you have as a community bank to your advantage. Whereas national lenders may come and go, your community wouldn’t be what it is without you there.

Strive to make lending and customer service decisions that benefit you, your clients, and your community—even if they require a little more time and effort—because they’ll pay off in the long run.

Your community bank is essential. You likely serve a group of clients that’s overlooked by larger banks. You’re part of a complex and stressful ecosystem. The balance is hard to strike—you must adopt the right resources to serve your clients without losing the human touch that separates you from other banks.

The days when “community bank” was synonymous with “small bank” are long gone. Consolidation and other outside threats loom. You must learn to create healthy growth without losing your bank’s identity.

On the merger and acquisition side, it’s an insanely complicated and trying process (especially your first time around). Simply put, it’s eat or be eaten.

So let’s concentrate on organic growth—marketing your bank to more clients within your footprint while slowly expanding those geographic boundaries. How do you strike a healthy balance of loan growth while controlling funding of deposits to maintain the yield that delivers profits to your institution?

The secret to marketing is simple: tell more people better. Good news—this doesn’t require a huge budget. It does require commitment, some experience, and at least a little expertise.

You can expand over time, but every minute you wait to start, you lose ground. Maybe you’ve started, but you’re stuck. You’re not beating the competition, and you don’t know where to go.

We see many, many ways in which banks are wasting money, time, and human capital. If you feel you’re squandering opportunities, you might be guilty of one (or more) of these 10 cardinal sins:

1. You truly don’t see the value of marketing.

The success of most community banks has been based on shoe leather and handshakes. Personal relationships are directly proportional to asset growth. But what happens when that stalls—when the big bank de-novos into your community, cuts loan rates, and boosts deposit interest? When you’ve pressed the flesh for your whole career (and it’s worked really, really well), it’s hard to see the value in increasing an expense line item.

I understand. You may not be adversarial to marketing. You simply don’t understand it.

Too many banks approach marketing by just checking the box. An admin person gets a “promotion” and a “budget,” then is expected to perform. Perhaps you send them to some training. However, the expense line item bugs you and you’d really like to see some ROI.

The fix:

Commit, but start slow. Understand that, in the beginning, a marketing department doesn’t run a P&L—it’s an expense. Allocate a budget you’re willing to spend. Set goals and determine a path toward accomplishing those goals. If you and your staff genuinely have no idea where to begin, hire some help. Yes, it’s self-serving for an agency to make this recommendation; but it’s just true.

2. You don’t know how to do it.

It’s hard to admit, but ignorance is the number-one reason for failures within bank marketing. It’s tough to get traction if you and your staff don’t know what you’re doing. Moreover, you’ll only make it worse because you will damage the belief in marketing as a valid activity.

If you fall into this category, I won’t beat you up.

The fix:

It’s simple (and a bit self-serving): find outside help. It doesn’t have to be Mabus Agency (but we are the best option). The money spent with a qualified agency can help you experience early wins that return revenue to the bank, fund future activities, and increase confidence in your efforts.

3. You convince yourself you don’t have the budget to compete.

Inaction is second to ignorance in creating failure within financial marketing.

Don’t psych yourself out. Being the underdog might be a better position than you think. In his book, “David and Goliath,” Malcolm Gladwell makes the point about the eponymous story, that David likely had an advantage over his larger opponent. Gladwell posits that David’s youth, stealth, and accuracy from practice with a sling made him the perfect enemy of the larger, slower-moving giant. Because David was not seen as a threat, he was able to get into position and fire while Goliath scoffed. (I highly recommend this book.)

David won because of his size. Not despite it.

Our work with banks proves that “bigger” doesn’t always mean “winner.”

The fix:

Concentrate your limited resources on your most significant opportunity. Everyone has less of a budget than they want or need. You must get used to concentration—and exercise the ability to say no to compelling opportunities that might seem like a decent fit. You must reject activities that spread your resources too thin.

4. You don’t want to poke the bear.

First-time marketers often worry about the consequences of their efforts:

“If I start marketing, will others just spend more money?”

“Will it escalate out of control?”

“Maybe the competition will drop/increase their rate.”

If you’re trying to fly under your competition’s radar, you’re probably flying under your potential clients’ radar, too.

Hopefully, it’s apparent that this is not a winning strategy.

The fix:

You don’t have to get in your competitors’ faces to advertise. Tell your story. Again, the trick is doing better today than you did yesterday. You don’t have to compare yourself to the competition, but if you have something that sets you apart, you can (and should) brag on that item. Regardless, you can’t live your marketing life in contrast with another financial institution. You must understand your competitive environment, then execute your own plan.

5. You’re too busy copying them.

They put an ad in the newspaper. Why aren’t we in the newspaper?!

They sponsored a community event. Why weren’t we the sponsor?!

They put their bankers in an ad. Why didn’t we?!

If you’re chasing your competition like this, you’ll never catch up. Bankers just like you, all over the country, face undue stress related to tactics like these. I believe this tendency is derivative of that same competitive letdown you feel when “they beat us for that loan.” It feels like a loss.

Marketing like your competition only depletes valuable energy and leads to homogenized advertising environments that are less effective for all financial institutions.

The fix:

Zig when they zag. When your newspaper rep calls and says, “…but every other bank will be in this publication…,” I want you to grit your teeth and say, “NO.” It will be tough in the beginning, but you must understand that it does you no good to be diluted amongst every other bank. You have to convince your bankers that you’re not missing out by being the only bank missing from a Chamber of Commerce welcome bag containing seven other banks’ promotional items. But it’s not about sitting on the sideline. Your competition is zagging. What are you doing to zig? Own a premium ad position in a key publication (that’s not littered with banks). Commit to a strong billboard message. Show up where you can stand out, and own that platform.

This is a real-world example. A Chamber representative brought this welcome bag to a branch opening. What good does this do any of these banks?

6. You’re buying what THEY’RE selling

I had an epiphany while attending a recent bank marketing event.

I walked through the tradeshow floor and surveyed the vendors.

Represented were a couple of sales tools (CRMs), personal financial management systems, and lots of digital signage vendors. All of these represented activities that start after a potential client engages with your institution.

Where was all the stuff that attracts a new client? Nonexistent. Absent. There were no digital media representatives. No traditional media. Only a bit of social media.

The problem is that we assume what we’re being shown is what’s important, and it’s what we should be considering.

If you engaged every vendor at the event, you’d still be missing a valuable component: how to attract new clients.

The fix:

Make sure you utilize techniques designed to attract new clients. Yes, it’s important to nurture clients and deepen relationships. However, you first have to make certain new clients are coming in. The great news for you? If your competition hasn’t adopted this philosophy, you might be the only one marketing in your trade area.

7. You admire them too much.

The relationships amongst bankers drive me a bit nuts sometimes. Bankers will compete like bitter enemies over a single loan or client relationship. However, when it comes time to market against the bank down the street, a banker will say, “I’m just not going to do that to him/her.”

It’s like a strange code of honor—one I don’t understand.

This attitude is shrinking, but it’s still around. I’m all for friendly competition, but competition is the keyword. Make certain you’re competitive.

The fix:

Play golf at the annual event with your competitors, but maintain a healthy marketing plan. You don’t have to denigrate your competitors to market, but you have to gain awareness amongst your potential clients.

8. You’re in the industry trap.

Bank-specific vendors do a great job scaring you to death about compliance and security. Then they turn around and charge you based on those fears.

Security and compliance are vitally important, but sometimes, the focus on financial-specific solutions obscures other solutions outside the “built-for-banks” marketplace.

There is a limited pool of bank vendors, so we all wind up using the same tools. Community banks are dependent on outside companies to develop software and solutions. The biggest pain point is when your institution outgrows its current solution, but you’re stuck in a contract.

The fix:

Vet thoroughly. When adopting a new software or solution, we suggest bringing in at least one potential solution from outside the financial world. Even if an outside-the-industry solution doesn’t fit, it might enlighten you to functionality you wouldn’t have known existed.

9. You think bankers are more important than brand.

Want to close the browser? Hang in here with me, because you need to read this more than anyone else. Bankers are infinitely valuable to the banking process. Absolutely. However, when stepping into the world of advertising, putting bankers in an ad is less important than building a brand.

I’ve seen banks spend thousands of dollars building the “brand” of an individual banker. Then that banker (along with his/her portfolio) was lifted out. The new bank didn’t have to pay to build that banker’s following—just a salary it was willing to pay anyway.

Also, bankers seem to think that consumers like to see bankers in ads. A consumer might value a personal relationship with his/her banker. However, a client appreciates a strong institution more than a relationship with a single banker. If you don’t believe that, you probably haven’t worked in one of those strong institutions.

The fix:

When you pay to build your brand, that investment persists beyond bankers who come and go. You build a foundation that communicates strength to a brand-centric culture. You can attract more bankers in the future. In short, you win.

10. That’s just not what community banks do!

Hahahahahahaha.

The fix:

Either shut the doors or sell. Otherwise, we’ll meet when one of your competitors hires us; and you don’t want that.