As a bank marketer, you see the differences.

You see charter types and product mixes.

You see community involvement and lending philosophy.

You see the heart behind the service.

But to most customers?

They just see a bank.

A building.

A logo.

A place to keep their money—until something goes wrong.

When the differences aren’t obvious, the choice doesn’t feel meaningful.

So most people don’t make one.

They don’t move.

Not because they’re loyal.

Because everything else looks the same.

That’s the real challenge:

They’re not actively choosing your competitor.

They’re just not seeing a reason to choose you.

The Sea of Sameness (And How We Got Here)

You’ve felt it.

You’ve seen your competitor’s ad and thought,

“That could’ve been ours.”

You’ve heard your CEO say,

“Can we do something like what [other bank] is doing?”

And you’ve probably even asked your agency,

“Can you show us what’s working for other banks?”

That’s not a failure. It’s a survival instinct.

Banking is conservative. Regulated. Reputation-driven.

You’re expected to be safe.

But “safe” becomes a trap.

It’s what leads to this moment:

You finally get buy-in for a bold, original campaign.

It’s on-brief. On-brand. And actually different.

You show it off.

And the first question someone asks is:

“Can you show us where someone has done this before?”

That instinct—understandable as it is—is the root of the sameness problem.

You’re not copying others because you lack creativity.

You’re copying others because you’re afraid to go first.

The Illusion of Safety

It’s easy to feel like fitting in protects your brand.

But it actually weakens it.

You’ve probably heard or said things like:

- “Let’s not go too far with this.”

- “We want to be different—but not too different.”

- “We need to sound like a bank.”

Those phrases might help you avoid risk.

But they also make it harder for anyone to tell your story—or remember it.

And from the customer’s point of view, everything starts to blur.

What Your Customers Might See

You might have a brand with real depth—a distinct personality, clear values, and a meaningful story.

But that doesn’t mean your customers are picking up on it.

If your outward expression isn’t pulling its weight, you might be unintentionally blending in.

That can happen with:

- A logo that doesn’t feel as different as it could

- A color scheme that shows up in half your competitors’ ads

- A name that sounds just like ten other banks in your region

Individually, none of these things are deal-breakers.

But together, they can make your brand harder to distinguish—especially to someone who isn’t looking closely.

And most people aren’t.

They’re busy. They’re scanning. They’re looking for something that feels relevant, clear, and maybe even a little refreshing.

If your brand doesn’t make that impression quickly, it may not get a second chance.

What Actually Stands Out

You don’t need to be flashy.

You just need to be clearer than the other guys.

Customers don’t want clever.

They want something that makes sense—something that feels right.

That means:

- A homepage that gets to the point

- A campaign that reflects real people, not polished stock photos

- A tagline that speaks to something your audience actually feels

- A tone that sounds like someone—not something

Your job is to find the small nuance that sets your bank apart—

and magnify that nuance until it becomes unmistakable.

You don’t have to be loud.

You just have to sound like you—and only you.

That alone makes a difference.

Proof It Works

We’ve helped banks step out of the sea of sameness—and we’ve seen what happens when they do.

- One focused its brand entirely around serving a coastal region

- Another leaned into its commercial DNA and stopped trying to be everything to everyone

- A third turned its limited tech stack into a strength in customer responsiveness

- One bank proudly led with its rural identity and made it a calling card

- And another broke through with a voice that was bold, clear, and still deeply human

None of them stood out by being trendy.

They stood out by being true.

You Don’t Need a Revolution—You Need to Zig

The next time someone says,

“Every other bank is doing this,”

Your answer should be:

“That’s a good reason for us to find something more original.”

Because when every other bank is zagging, your best move is to zig.

Familiar brands fade into the background.

But brave ones don’t just attract attention. They earn trust.

And they give customers something they haven’t had in a while:

A real reason to move.

So go ahead—make your move.

Say what only your bank can say.

Say it like you mean it.

And let the others keep blending in.

You’ve got better things to say.

Everyone says it.

Every bank. Every billboard. Every website.

Better service.

Like it’s fresh. Like it’s compelling. Like it’s going to turn heads.

But no one walks into your bank and says,

“I’m here for better service.”

They’re there to open an account. Secure a loan. Solve a problem.

And here’s the truth:

“Better service” isn’t a brand.

It’s not even a differentiator.

It’s the baseline. The status quo.

It’s what customers expect—not what sets you apart.

In a category as crowded and inertial as banking, that’s not just a messaging issue.

It’s a problem that can prevent growth.

The Comfort of the Familiar

“Better service” is easy to say because it feels true.

You know your team works hard. You know customers like you.

So why not lead with that?

Because it’s not a messaging strategy. It’s a safety blanket.

And when your competitors all say the same thing, it loses its meaning.

Drive around town. Look at billboards. Browse a few bank websites.

You’ll see it again and again:

- Where service matters.

- Banking with a personal touch.

- Real people. Real service.

These aren’t differentiators. They’re wallpaper.

The Cost of Vagueness

When everyone says the same thing, no one stands out.

“Better service” becomes background noise. It blends into the landscape.

Worse, it creates a burden of proof you can’t deliver in a slogan or a homepage headline.

It also opens the door to disappointment.

Because what does “better” mean?

To one customer, it’s faster turnaround.

To another, it’s empathy.

To another, it’s not having to come into a branch at all.

If you don’t define it, your audience will.

And they’ll define it against their last bad experience.

When that happens, banks unintentionally set traps for themselves.

They make a promise they haven’t clarified. And when reality doesn’t match the customer’s expectation, trust erodes.

What “Better” Actually Sounds Like

You don’t need to stop offering great service.

You just need to say it differently.

You don’t need to kill the word “better.”

You need to show what your version of better looks like.

Try these reframes:

Instead of: We offer better service.

Say: Your banker answers when you call.

Instead of: We’re here when it matters most.

Say: Open your account in under 10 minutes—online or in-branch.

Instead of: We put you first.

Say: Decisions made in this ZIP code—not at corporate.

Each one replaces a vague aspiration with a vivid reality.

It’s not about being louder. It’s about being clearer.

And it’s this kind of clarity that sets the stage for one of the best recent examples of specificity in service messaging.

The Role of Strategy

Banks don’t default to “service” because it’s bold.

They default to it because it’s familiar, and because they haven’t made a strategic choice about what they want to own.

This means you have to make decisions. You have determine what to actually claim as a benefit.

It means knowing your strength and leaning into it while letting go of the rest.

If your differentiator is responsiveness, prove it.

If it’s relationships, show how those relationships create better outcomes.

If it’s speed, quantify it.

Strategy doesn’t hem you in. It gives you room to move with intention.

Reframing the Message

Think of your messaging as translation.

The customer says: “I’m tired of waiting.”

You say: “Get a loan decision in 48 hours—or less.”

They say: “I feel like a number.”

You say: “You’ll never have to explain your situation twice.”

You’re not describing your team. You’re addressing real friction.

You’re not listing features. You’re reframing the relationship.

And in doing that, you offer something much stronger than “good service.”

You offer relief.

The Real-World Shift: First National Bank of Central Texas

First National Bank of Central Texas (FNBCT) operates in Waco, right in the heart of Texas—a market crowded with good community banks and even better bankers. Word-of-mouth was strong. Their team was respected. Their reputation was solid.

But as they expanded into new markets like Bryan and College Station, reputation wasn’t enough.

People didn’t know them.

And saying “we have great service” wouldn’t cut it in a market where every community bank could say the same.

So we listened.

Their bankers weren’t just friendly or responsive.

They took ownership of the process.

If a loan didn’t go smoothly, they felt it personally.

If a business owner hit a snag, they were the one picking up the phone to clear the path—not pointing to red tape.

This wasn’t service. This was partnership.

The brand line became:

“A bank on your side. A banker by your side.”

It resonated immediately. Not just with leadership. With the bankers themselves.

It wasn’t a clever twist. It was a mirror.

And most importantly, it gave customers something real.

Because banking often feels adversarial—especially for small business owners.

The process can feel like an interrogation:

How do you plan to make money?

Have you thought about this risk?

What if this fails?

This message flipped that dynamic.

Instead of feeling scrutinized, customers could feel supported.

And that subtle shift—from scrutiny to support—is where trust begins.

When Everyone Says They Care

Let’s be honest—every bank says they care about their customers.

But caring is a minimum requirement, not a market position.

The real differentiator is what your care looks like in practice.

Do you simplify?

Do you expedite?

Do you stand beside your customers instead of across the table from them?

If so, show that.

Not through generic declarations—but through tangible promises.

“A banker by your side” is more than a phrase. It’s a structure.

It sets expectations. It defines the relationship.

And that’s what branding is supposed to do.

Final Thought: Let Your Competitors Say “Better”

The next time a competitor rolls out a “where service matters” campaign, take it as a gift.

They’ve just opted out of the race for relevance.

While they’re busy blending in, you’ll be building clarity.

Confidence. Connection.

Customers don’t want platitudes.

They want to know you see their problem—and have a real way to fix it.

“Better service” fades.

But “A banker by your side”?

That sticks.

And a bank on your side too?

That’s not just a message—it’s a mindset.

One that turns vague promises into real expectations.

One that makes people feel something—and remember who made them feel it.

Don’t just say it louder.

Say it smarter.

Say what only you can say.

Then go prove it.

5 Banking Archetypes that Beat Marketing Personas

Marketing loves personas. They show up in ad briefs and strategy decks with names like Savvy Sarah or Budget-Conscious Ben, complete with stock photos and imagined lifestyles. They’re neat. They’re tidy. And they’re absolutely useless.

Here’s the problem—personas aren’t real people. They’re flimsy composites based on assumptions, not behavior. They don’t reflect how anyone actually makes decisions, just a mood someone might be in at any given moment. And in banking, that’s not good enough.

Worse yet, personas aren’t even created to help banks—they’re created to sell something to banks. Vendors design them as a “helpful” shorthand, a way to package insights into something digestible. But strip away the stock photos and vague demographic details, and what’s left? A vacuous model designed by people who’ve never actually worked in banking. A concept that sounds smart in a pitch deck but collapses under scrutiny.

And even if personas were meaningful, their logic is fundamentally broken. Most persona models include eight, ten—sometimes dozens of different profiles. How exactly is a bank supposed to create a cohesive brand strategy when it’s being asked to speak to that many audiences at once? It’s an impossible task. You end up either segmenting yourself into oblivion or creating generic messaging that means nothing to anyone.

This is why personas fail. They assume, they generalize, and they force banks into unsolvable marketing problems.

What actually matters is why customers leave their banks. Customers don’t leave banks because they fit into some marketing persona. They leave because something broke—trust, service, or convenience. When frustration builds to a breaking point, they walk.

These failures aren’t random. They follow patterns.

This is where archetypes change the game.

Instead of trying to market to made-up personas, you focus on the five real reasons customers break up with their bank. These archetypes aren’t neat little labels that fit into a PowerPoint deck. They are raw, emotional states of dissatisfaction—the tipping points that push customers to walk away.

When you align your brand messaging to these archetypes, you aren’t just “marketing.” You’re speaking directly to the only customers who are ready to move.

Let’s break them down.

Banking Archetypes

Archetype 1 – The Unseen

Their bank knows nothing about them. There are no efficiencies gained in their transactions from an understanding of the individual as a customer. Their bank isn’t asking relevant questions (or storing the answers) to provide guidance, insight, or product suggestions that will help the customer advance their financial position. The bank also doesn’t possess or utilize local knowledge to provide similar help and efficiencies.

To this customer, it’s as if they’re invisible. Each interaction is transactional, sterile, and devoid of personal connection. Imagine walking into a place that claims to know you—to serve you—but instead, you’re treated as though you’re a complete stranger every single time. The questions that should reveal your goals, dreams, and financial anxieties are absent. The tools that could make life smoother remain untouched because no one bothers to ask what’s needed.

How the personality might express their frustration:

“The bank feels lost or out of touch with me. I feel like I must explain myself every time I transact. I’m not getting the help I need from my bank.”

Archetype 2 – The Afterthought

Their bank does not value their time. The bank opens after the customer gets to work and closes before they get off. The customer has to sacrifice a lunch break or take time off from work to visit the bank. It is difficult to find what a customer needs on the bank’s website. It is difficult to get a real person to contact you. Everything feels highly inefficient.

How the personality might express their frustration:

“I feel like I must sacrifice my time to transact with my bank. My bank does not value my time.”

Archetype 3 – The Tangled

The bank makes the customer undertake convoluted processes that benefit the bank at the expense of the customer’s valuable time. It is complicated to apply for loans or sign up for checking accounts—either in person or online. Accomplishing anything with the bank feels unnecessarily complex.

How the personality might express their frustration:

“It feels like the bank is willing to waste my time to make their jobs easier. I know there must be a simpler way to bank.”

Archetype 4 – The Postponed

The bank does not meet the customer’s level of commitment, energy, or pace. Every customer needs fast answers to make decisions. Some banks feel like they’re dragging their feet, causing real consequences.

How the personality might express their frustration:

“I feel like I’m always waiting on my bank. I’m waiting on an answer or for their app to work. I feel like the world is passing me by.”

Archetype 5 – The Estranged

The bank doesn’t feel like it is built for the customer. Nothing about the bank is congruent with a customer’s lifestyle. Maybe their mobile app, online banking, or in-person processes are outdated and antiquated. Maybe they’re too “high-tech” to even make sense. Everything can feel adversarial—even personnel.

How the personality might express their frustration:

“My bank doesn’t feel like it’s built for me. I don’t ever feel comfortable interacting with my bank. It doesn’t feel like my bank is on my side.”

The Opportunity: Tailored Solutions for Archetypes

When someone is frustrated enough to leave their bank, they’re not just looking for a new “vibe” or a bank that aligns with a “carefully crafted” persona. They’re looking for a solution to a problem.

And here’s the real problem with personas: they assume too much and understand too little. They take a few surface-level characteristics, slap on a name, and pretend they’ve captured something meaningful. But no one wants to be reduced to a marketing stereotype.

This isn’t just a shift in perspective—it’s a shift in power. When banks stop thinking in terms of personas and start thinking in terms of archetypes, they stop reacting to generic market trends and start proactively solving real customer problems.

Because at the end of the day, customers don’t want to be treated like Savvy Sarah or Budget-Conscious Ben. They don’t want a bank making shallow assumptions about their needs based on an imaginary profile.

They want a bank that actually understands them, values their time, and solves their problems.

And the banks that embrace this approach? They’ll win. Because they’ll be the ones listening when everyone else is just guessing.

Bonus Content: How to Message to Archetypes

We can’t just diagnose the problem. We must deliver some solutions—or at least some suggestions.

Understanding why customers leave their banks is only the first step. The real opportunity lies in how you communicate that understanding. Your bank’s messaging should be a direct response to the frustrations that drive customers to switch. It should cut through the noise and speak to the moment of decision—the exact point where dissatisfaction turns into action.

To help, we’ve outlined suggestions for how a bank might position itself as the solution to each archetype’s frustration. While these are generalized examples any bank could use, they aren’t generic. Each message is crafted to resonate with customers in the precise moment they’re ready to move—not just to attract attention, but to make switching banks feel like the obvious next step.

For The Unseen: “Your bank should know you—not just your account number.”

Tired of repeating yourself every time you visit your bank? It’s frustrating when your financial institution treats you like a stranger instead of a valued customer.

We believe your bank should know your goals, anticipate your needs, and offer real solutions—not just transactions. From personalized recommendations to local insights that actually help, we make banking feel like a partnership, not a process.

Are you tired of feeling unseen? It’s time for a bank that actually knows you.

For The Afterthought: “Your time matters. Your bank should act like it.”

Banking shouldn’t feel like an errand you have to plan your day around. Long lines, inconvenient hours, endless phone menus—if your bank makes you jump through hoops just to get things done, that’s the problem, not you.

We work on your time, not the other way around. Early morning, late at night, during lunch—we make banking effortless with extended hours, real human support, and digital tools that don’t require a tutorial.

Feel like your bank is stuck in the past? Maybe it’s time for a switch.

For The Tangled: “Banking should be simple. Not a maze.”

Why does opening an account feel like applying for a mortgage? Why does applying for a loan feel like a full-time job? If your bank makes simple things complicated, it’s time to ask: who is this process really serving?

We cut through the red tape. Fewer forms. Faster decisions. Straight answers. Because banking shouldn’t feel like bureaucracy—it should feel like progress.

If banking feels like a headache, maybe you need a bank that works for you.

For The Postponed: “Opportunities don’t wait. Neither should your bank.”

A slow bank isn’t just frustrating—it can cost you real opportunities. A delayed approval or sluggish loan process means you might lose out. You don’t have time to wait.

We move at your speed. Fast approvals. Real-time decisions. Digital tools that work when you need them. Because when your bank moves at your pace, you win.

If you’re always waiting on your bank, maybe it’s time to move on.

For The Estranged: “Your bank should feel like it was built for you.”

If your bank’s app is clunky, its processes outdated, or its service feels robotic, it’s easy to feel like you don’t belong. A bank should work with you, not against you.

We design banking for real people. Intuitive tech, seamless in-person experiences, and customer support that actually supports you. Banking should feel effortless—not like an uphill battle.

If your bank feels foreign, maybe it’s time for one that feels like home.

We bank marketers are constantly plagued with a burning question: how do I split my ad dollars between brand and product advertising? I know I need to strengthen my bank’s brand, but I have line-of-business leaders breathing down my neck to run product ads.

Instead of burying the information like an online recipe, I’ll cut to the chase and answer you right here. You should spend at least 70% of your budget (creative and media) on brand advertising.

Why?

Your brand is how you show people why your bank floats above the rest in a sea of sameness. Well, that’s only if you’re correctly messaging your brand.

You need to understand that your largest group of potential customers at any given time is made up of people who’re upset enough at their current institution to go through the catharsis to change banks. Your potential customer isn’t thinking about how many ATMs you have or what your app looks like. They want to know if your app works. They’re desperate to know if someone will be there to help if something breaks. They want to know how their experience at your bank will be different than their current bank.

It’s not about features—it’s about feelings

Product advertising dominates the conversation at many banks, focusing on the newest innovations—to spend advertising dollars to support the dollars invested in technology. Brand advertising is often dismissed by bankers as vague or less tangible. “We paid for these products! Why are we just talking about the bank!?” But advertising products rarely differentiate one bank from another—they’re expected.

- In the 1980s, banks spent millions installing ATMs. Then they spent millions more promoting them.

- Later, it was debit cards.

- Into the 90s and early 2000s, it was online banking.

- Then came mobile banking.

- And lately, PFMs, ITMs, and “value-added” DDAs.

Each time, banks invested heavily to keep pace with competitors and then launched campaigns promoting their new products. The result? The bank told the customer what made it the same as every other bank.

Let’s be honest with ourselves: No one switches banks because of an ATM, a debit card, or mobile banking. These are expected features of any modern bank. People only leave their bank when they’re so dissatisfied that they can no longer tolerate it—when their frustration outweighs the inconvenience of switching. And switching banks is inconvenient. It’s like being stuck in a leaky boat—you might try to endure, but once the water rises past your ankles, you’ll jump in and swim.

But in that sea of sameness, where do you head? To the bank that promises the experience you desire.

Branding is the backbone of your advertising strategy. When done well, builds the case for the reason why someone would choose your bank. Sure, one bank is similar to another. But our job is to find the nuance that separates our bank and to magnify those subtle differences. Our job is to give the potential customer a reason to choose our bank. Brand advertising requires a shift in perspective—from thinking about products to thinking about people. It’s not about what you offer; it’s about why you matter—specifically when things are going wrong in someone’s life.

Your Ads Don’t Have to do All the Work

Another item you must understand: your ad is only half of the equation. The other half is your audience. Your audience is a mosaic of individual needs, concerns, and aspirations. As we stated earlier, someone will only entertain your bank when they’ve had enough at their institution. Unless we want to reopen the debate of banking the unbanked, and I’d rather not.

Your audience brings their own needs, worries, and dreams into any ad that’s good enough to stop them and engage their minds. Effective ads don’t just speak; they listen. They answer the readers’ questions. They acknowledge their worries. And they reassure them we have the banking experience you’ve always wanted.

Perhaps the best way to communicate this is through an example. Think of these two scenarios:

Amelia, a single mom, is busy raising her daughter. She works a ton to make sure her daughter has everything she needs, but she also spends as much time as possible with her little girl. Her bank has messed up three of her last seven direct deposits. While she’s not living paycheck to paycheck, it does cause her to worry each and every pay period. “Will have I have to wait on my bank to get it together this time to make sure my paycheck is available?” She’s called the bank several times, and no one can identify the problem. It feels like they’re passing the buck to her employer, but Amelia has asked her coworkers. None of them have experienced the same issues with their banks.

Amelia’s looking for a new bank. But it feels like she has no spare time to truly compare institutions.

Grant has owned his own business for 20 years. He’s been planning to expand for the past three years. The timing is finally right. The equipment he needs has advanced sufficiently to meet his needs. Building materials are reasonable, and the lot adjacent to his current location has come up for sale. He’s met with two banks, but he’s had to call them each week to get any update. One banker says he’s waiting on his credit department. The other banker keeps asking for other sources of income and collateral but aren’t really communicating what’s missing. Grant’s not getting enough answers, and he’s worried the opportunity will slip by.

Grant’s looking for a new bank. But he’s busy running his business, and he’s worried that every bank might just be the same.

Now, let’s say we put the same ads in front of Amelia and Grant.

Ad A is a retail-centric ad. It talks about branch and ATM locations. It mentions cashback checking and customizable debit cards. This ad should perform better for Amelia. She’s looking for a retail bank, after all. But, likely, Grant will tune out. He’s looking for a business bank.

Ad B is a business ad. It talks about competitive rates and local decisions. It mentions a local lender (with her picture!). Grant should be more interested in this ad. Maybe he’ll give them a chance to bid on his loan. Meanwhile, this doesn’t look like a bank for Amelia.

Let’s consider a third ad—a brand ad that captures the bank’s core values—dedication, responsiveness, and care. This ad should resonate with both Amelia and Grant. They both feel like their existing bank left them out in the cold. The right brand ad will speak to their pains and let them know they’ll be taken care of.

Amelia and Grant aren’t just looking for features; they’re looking for solutions to their frustrations. What they want, what they’re desperate for, is a promise of something better—a bank that listens, cares, and takes action.

Think of a brand ad as a universal translator. It doesn’t matter if the customer is upset with a botched paycheck or a stalled business loan—the ad speaks to their frustrations and promises a better way forward. This is the kind of connection that great branding creates. It’s not about listing features or pitching products; it’s about saying, “We see you. We hear you. We’re here for you.”

But what happens after that? Community banks, in particular, pride themselves on putting the customer first. If your bank really believes and practices this, it will attract a customer with its brand, and let the customer decide which product or service to adopt.

So, you’re saying, even if we’re trying to sell checking accounts, we should be happy if a business lending customer comes in from our ads?

Hell yes.

When you have a chance to attract a new relationship, you attract them. You meet the customer where they are, and you serve them. Then you comprehensively onboard that customer—letting them know what all your bank has to offer. This sets you up to use email and other platforms to nurture (cross-sell) the other products.

Yes, it’s a longer approach. But you can’t squander an opportunity to attract a new customer. Plus, you were never going to attract someone with a checking account ad that was looking for a loan. If this doesn’t resonate with you, I’m truly, truly sorry for you and your bank.

A true client-first approach means serving the customer to make their lives easier and their banking relationship more valuable. With thoughtful follow-ups, email nurturing, and targeted digital outreach, you’re not just adding products—you’re embedding yourself into their daily lives. You’re helping them reach their goals. This isn’t just retention; it’s relationship-building at its finest.

Budget Allocation: The other 30%

So, we said 70% toward brand. What about the rest? Allocate 20% to line-of-business advertising. This shows that you’re a retail bank, a business bank, and a mortgage bank. Use the remaining 10% on product advertising to promote specific offerings, but only as part of a broader, brand-centric strategy. These ads are the accents on the masterpiece, not the canvas itself.

In banking, trust and connection are everything. People move when they feel abandoned or unheard. Your brand is your promise that things will be different—that you understand who they are and what they need. It’s paramount that you’re able and willing to articulate the nuance that sets your bank apart. That’s the bridge between frustration and hope. And you have to back this with ad dollars.

No one asks, “Where do you deposit or your money?” or “Where is your checking account?”

The question that one customer asks another is, “Where you bank?” And the follow-up is,

“Are you happy there?”

What does your bank do to make your customers happy? Do you make them feel more cared-for than their current bank?

At its heart, advertising is about connection. It’s about taking the essence of your institution and making it resonate with real people. Don’t squander this opportunity. Use your brand to tell a story of trust, reliability, and care. Because, at the end of the day, products don’t build loyalty. Relationships do.

Ads are two-way conversations.

Every ad shares one critical element.

And yet, almost everyone misses it.

Do you know what it is?

Here’s a riddle for you:

I am many, yet unseen,

Clicked and scrolled on every screen.

Each mind unique, each heart its own,

In my numbers, your brand is sown.

What am I?

The audience.

Wait—seriously? Everyone forgets the audience?

Yep. Let me explain. Sure, you analyzed the audience. You assessed the demographics. Maybe you sliced the data and targeted the right behaviors. You’re confident the ad got to the exact right place. But here’s the problem: When it comes time to actually speak to that audience—or more importantly, the individuals who make up that audience—you fumble.

It’s a classic mistake in marketing. We focus so much on finding the audience that we forget to actually speak to them as individuals. The result? Ads that are technically precise but emotionally flat. Ads that miss the mark—not because they’re in the wrong place, but because they don’t resonate with the people they’re supposed to reach.

You’re Not Talking to a Crowd—You’re Talking to a Person

This article is a bit of a spiritual sequel to one of my earlier pieces, “One Tip to Boost Your Writing,” wherein I emphasized writing to an individual rather than an audience. If you haven’t read it yet, let me sum it up: People don’t consume your ad as part of a group. They experience it as individuals. Your billboard? It’s read by one set of eyes at a time. Your Instagram ad? It shows up on someone’s personal feed. Every piece of marketing, no matter how widely distributed, feels personal when it’s consumed.

But here’s the thing: The previous article only scratched the surface. Yes, writing to an individual is critical. But there’s more to it. What’s missing? The conversation.

The Missing Piece: A Conversation

When you write an ad, you’re not just sharing information. You’re starting a dialogue—at least, you should be. But too often, ads don’t feel like conversations. They feel like lectures. They overtalk. They assume. They forget that every member of the audience brings their own unique experiences, perspectives, and emotions to the table. And that matters.

Let’s make it specific to bank marketing, where this problem becomes even more glaring. Think about an ad for a checking account. The only person it will resonate with is someone who’s actively looking for a new checking account. And let’s be honest: No one is switching banks on a whim. They’re switching because they’re frustrated—because they’re so fed up with their current situation that they’re ready to deal with the hassle of transferring bill pay, changing auto drafts, and starting a new banking relationship. And all of this when they’re not even sure the new bank will be any better. Yet, how many ads actually address that frustration? How many ask the simple but effective question: “Hey, are you fed up with your bank?”

It’s the same story on the commercial side. Business banking customers are inundated with pitches from lenders at other banks. They don’t lack options. But they do lack trust. To even get on their radar, you need to acknowledge their pain points. Maybe their current banker didn’t show up on time or wasted their day with unnecessary delays. Maybe they feel like no one truly understands their business. Whatever it is, you have to speak to those frustrations. If you don’t, you’re just noise.

What Does a Conversation Look Like in an Ad?

So, how do you turn your ad into a conversation? It’s not as complicated as it sounds. Here are a few key principles to keep in mind:

- Acknowledge Their Perspective

Remember, your audience isn’t a blank slate. They’re bringing their own experiences, challenges, and desires to the table. Your ad needs to speak to that. Ask yourself: What do they already know? What do they care about? What are they feeling right now? - Use Simple, Relatable Language

The best conversations aren’t stuffed with jargon or over-polished sentences. They’re real. They’re human. Your ad should sound like something you’d actually say to a friend—not like a robot reading a sales script. - Focus on Them, Not You

This one’s huge. Your ad isn’t about your brand. It’s about what your brand can do for them. Instead of saying, “We offer the best rates in town,” try, “You deserve a bank that helps you save more.” - Address Their Problems

Don’t just talk about features—talk about the frustrations your audience is facing. Are they tired of a banking app that never works? Exhausted from chasing down a banker who doesn’t answer the phone? Put those frustrations front and center. - Invite Engagement

A conversation is a two-way street. Even if your audience can’t literally talk back to your ad, you can create a sense of interaction. Ask a question. Make a bold statement that invites them to mentally respond. Give them a reason to feel involved.

Banking Is Personal—Your Ads Should Be, Too

Banking is personal. A checking account isn’t just a product—it’s an essential part of our life. A business loan isn’t just a number—it’s someone’s dream of growth, expansion, or survival. When your ads feel like conversations, you can build that personal connection. You acknowledge the struggles your audience is facing, and position yourself as the solution.

Start with One Simple Shift

So here’s your challenge: The next time you sit down to write an ad, don’t think about “the audience.” Think about one person. Picture them in your mind—they’ve just had a long day, juggling work and family, only to realize their bank’s app crashed when they needed to transfer money. Or maybe they stood in line at the branch for 30 minutes, only to be told they needed a document they didn’t have. What are they feeling? Frustration? Exhaustion? A little bit of both? What do they care about? Simplicity, reliability, and maybe even a sense of being valued. What do they need to hear from you? They need to know that your bank understands their struggles, that switching to you will make their life easier—not harder. Speak to that. Start a conversation that feels real, one that makes them think, “Finally, someone gets it.”

Bank marketing isn’t about shouting into the void. It’s about connecting—one person at a time. And when you focus on that, your ads won’t just get noticed. They’ll be remembered.

Banking has another pandemic looming as a threat.

It’s not a health concern, but it is a fast-spreading illness.

Customer service is dying across the country. And at a rapid rate.

Now, I’m not the first old white guy to shake my fist at the sky and proclaim such doom and gloom as a consumer. However, I’ll have you know that I love most of the things my peers complain about. I think advancements like self checkout are magical inventions. I don’t require human interaction to buy groceries—so long as my experience is easier.

This is not just one writer’s feeling. This decline in customer service is measurable. Recent data reveals that organizations globally are putting $3.7 trillion annually at risk due to bad customer experiences, an increase of approximately $600 billion (19%) compared to projections from last year. Customer service is getting worse and it is affecting profits.

The alarm bell I’m ringing for banks like yours deals with much darker patterns.

Dark Patterns

Have you ever tried to cancel your Amazon Prime account? It’s almost impossible to figure it out. Once you’re in, you’re in and you’re on auto-renew. It’s so difficult on consumers, the FTC filed a complaint against Amazon in 2023 decrying their practices of deceptive signups and difficulty to unenroll.

Here’s actual language from the complaint:

For years, Defendant Amazon.com, Inc. (“Amazon”) has knowingly duped millions of consumers into unknowingly enrolling in its Amazon Prime service (“Nonconsensual Enrollees” or “Nonconsensual Enrollment”). Specifically, Amazon used manipulative, coercive, or deceptive user-interface designs known as “dark patterns” to trick consumers into enrolling in automatically-renewing Prime subscriptions.

Dark patterns are systems used to manipulate users into making choices that are beneficial for the vendor but generally not ideal for the user. The term was coined in 2010 by user design specialist Harry Brignull. Amazon Prime isn’t the only example. Perhaps you purchased something online and noticed another service “snuck” into your cart before checkout (like a return fee or a warranty)? And these practices don’t just show up online, they’re creeping into the real world, too.

Dark Reality

Fortunately or unfortunately, I spend a lot of time on airplanes and in hotels. Both of these experiences continue to degrade, but have done so more rapidly lately than ever before. While airlines have long been the target of derision for customer service, the experience has gone from bad to almost adversarial. The most damning indicator to me is how similarly terrible the experiences are across airlines and hotels. Here are a few of the more concerning patterns:

The False Customer Service Desk

These are especially prevalent at airports. You miss a flight due to a delay, so you queue up to make sure you’re rebooked, etc. One airline made me scan a QR code to get into a virtual queue to then join the line. After the double wait, I get to the front only to find out that I have to call the customer service number to accomplish anything. I inquired, “Am I not at the customer service desk?” The reply: “No sir, we’re the help desk.” Well, ok.

App/Calltree Pickleball

So what happens when the “help” desk can’t actually help? You can always try the app. But there’s a reason this isn’t its own section—because most apps are useless for solving real problems. They rely too much on automation, rigid decision trees, and canned responses, which fall apart the moment a situation requires actual problem-solving.

You know you’re at a breaking point when the app tells you to call customer service—only for the automated system to insist, “Did you know you can resolve most issues in our app?” as if you haven’t already hit that dead end. This endless volley between app and call center is the corporate equivalent of a high-speed pickleball rally—except no one’s scoring points, and the only thing getting worn out is your patience.

At some point, we all break down into the universal customer service language of frustration: shouting REPRESENTATIVE! or OPERATOR! into the phone like a desperate incantation, hoping it will summon an actual human. And all of this happens when you’re stranded in an airport, scrambling for a hotel room, or just trying to get home. It would almost be funny—if it weren’t so infuriating.

The Buck Stops Anywhere but Here

No matter the platform the pervasive pattern is a combination of the ironic inability to actually help, no responsibility to solve any problems, and a huge lack of empathy for issues out of the customer’s control. After several issues with multiple airlines and hotels, I’ve left experienced feeling completely un-helped and literally stranded. I’ve stood across from other humans and felt absolutely powerless. Not only are these experiences common and similar across unrelated companies, but they feel designed. The processes feel designed to prevent help, reduce responsibility, and increase frustration to the point of giving up. If I had to guess (and trust me, I will) these occurrences not only feel purposeful, but created by the same organization. My best is on the large “accounting firms” who overreach into so many areas. While I have no true insight, I can see a soulless cash-grabbing consultant pitching a customer-centric business (such as airlines and hotels) to implement procedures that will save the company money, increase profits, and boost shareholder value. The problem is, though, they do this at the expense of the most valuable asset: the customer.

Banks Will Never Do That

But what does this have to do with banking? Community banks would never do anything like this, right? Hopefully not, but one thing I’ve noticed in a could of decades working with banks: trends in large corporations tend to eventually show up in banks—even smaller banks.

After all, look at chat bots. I’ve spoken to dozens of community banks across the country. When asked about their greatest strengths, the answer “our people” always ranks either first or second. The other response that shares the top spot is “customer service.” Yet somehow, vendors convinced quite a few community banks to add AI-driven chatbots to their websites. Why would a people-first, customer-centric community bank go against all logic and trust a robot to chat with its customers?

Well, I’d bet it was a really good vendor pitch deck that showed how other (likely larger) organizations were using chat bots. And that pitch was so good, it convinced a bank that a chat bot would actually help customers and be an extension of the bank’s awesome service—even though it makes no sense at all.

It’s a bit of a dark pattern in itself.

And it worries me that the same vendors who convinced airlines, hotels, and rental car companies that an initial bump to the bottom line would be worth it despite how it would frustrate their core customers will pitch similar “solutions” to your bank.

Hopefully, we’ll all remember that it’s not our people or our service that are our most valuable commodity. It’s our customers.

How to make sure your bank gets recommended—before the decision’s already made.

Someone’s sitting at their kitchen table, frustrated with their bank.

The app’s buggy. The customer service line bounced them around. Maybe the mortgage process dragged on longer than promised. Whatever the reason, they’re ready for a change.

So, they turn to someone they trust.

Not a spouse. Not a best friend. Not even Google.

They ask a new kind of advisor—one who never sleeps, never judges, and always seems to have an answer:

ChatGPT.

“What’s the best bank near me?”

“Who’s easiest to work with for small business loans?”

“Which banks still have people who answer the phone?”

This new friend doesn’t give a list of links to scroll through.

It gives recommendations.

A few banks. A few reasons. Enough to make a decision.

And if your bank’s not on that list—or shows up without a clear reason to choose you—someone else just won that relationship.

That’s where GEO comes in.

So, What Is GEO?

GEO stands for Generative Engine Optimization.

It’s not a buzzword—it’s how you make sure your bank shows up in AI-powered recommendations.

“Generative” refers to tools like ChatGPT (short for Generative Pre-trained Transformer)—AI engines trained to produce human-like responses based on what they’ve already read and trust.

These tools don’t crawl your site in real time like Google. They surface answers from content they’ve been trained on—and they favor writing that’s clear, specific, helpful, and confident.

If SEO gets you ranked, GEO gets you recommended.

Let’s be clear:

We’re not saying AI should replace your creativity, your instincts, or your strategy.

If you’ve read our past work, you know we’ve pushed hard for originality—for marketers to build skill, develop taste, and stay human in how they communicate. That hasn’t changed. In fact, our belief in actual intelligence is what fuels Mabus Agency. It’s why we write the way we do. It’s why our work works.

But something else is true, too:

Your customers are using AI.

They’re not asking you what makes your bank different.

They’re asking ChatGPT.

And if you don’t shape the answer, someone else will. GEO isn’t about writing for robots.

It’s about making sure the real, human value your bank provides is represented when AI tools speak on your behalf.

10 Ways to Make Your Bank GEO-Ready

(Each paired with its traditional SEO counterpart for context.)

1. Write like a human—everywhere.

SEO rewards keywords. GEO rewards clarity.

Nobody wants to read copy that sounds like it was written to game an algorithm. And ChatGPT won’t recommend it, either.

Where this matters: Homepage, service pages, product descriptions.

Do this:

Instead of: “Competitive residential lending solutions tailored to your needs.”

Say: “Buying your first home? We make the mortgage process simple—with low rates and fast answers.”

Make it sound like a person is talking to a person. Because one is.

2. Answer the actual questions your customers are asking.

SEO targets search terms. GEO mirrors real prompts.

People don’t search the same way they ask. Your content should match the way real humans speak when they’re frustrated, confused, or ready to act.

Where this matters: Blog posts, FAQ pages, product guides.

Do this:

Ask ChatGPT: “What are the most common questions people ask when looking for a [checking account, business loan, mortgage]?”

Then build pages that answer those questions directly.

3. Get specific or get skipped.

SEO values traffic. GEO values credibility.

If your copy is vague, AI tools skip it. They favor content that includes real stats, timelines, locations, and proof.

Where this matters: Testimonials, case studies, community stories.

Do this:

Don’t say: “We’re proud to serve our customers.”

Say: “In 2023, we helped 1,426 families close on homes—91% within 30 days.”

4. Structure your content like an actual guide.

SEO loves metadata. GEO loves logic.

Bold headers. Bullet points. Clear takeaways. These things help generative engines make sense of what you’re saying—and help readers do the same.

Where this matters: Landing pages, product breakdowns, explainer blogs.

Do this:

Use headers like “What to expect,” “Common pitfalls,” or “How to get started.”

Organize your information like a checklist, not a legal brief.

5. Say what you know—in your own voice.

SEO rewards length. GEO rewards insight.

You don’t need to write 2,000 words to win. You need to say something that sounds like you

know what you’re doing.

Where this matters: Blog posts, thought leadership pieces, about pages.

Do this:

Write like you’d explain it to a smart friend over lunch. Drop the jargon. Get to the point. Share what you’ve actually learned from helping customers.

6. Keep your content alive.

SEO favors freshness. GEO penalizes staleness.

Old content might still rank in search—but it’s probably ignored by AI. If your blog hasn’t been updated in two years, assume it’s dead weight.

Where this matters: Blog, resource pages, news updates.

Do this:

Set a calendar to update high-traffic or high-value content every 6–12 months. New numbers, new outcomes, new relevance.

7. Pair your name with your niche.

SEO gets clicks. GEO gets citations.

You want ChatGPT to associate your bank with something clear and positive: “great for first-time homebuyers,” “easy to work with for SBA loans,” “community-first bank with fast answers.”

Where this matters: Case studies, homepage, customer quotes.

Do this:

Say: “For 20 years, Riverpoint Bank has helped small businesses secure the funding they need to grow.”

You’re not just trying to sound impressive. You’re training the engine.

8. Tighten up your About and product pages.

SEO ignores bios. GEO quotes them.

Generative engines often pull summaries directly from your About page or product intros. Sloppy, vague copy here can do real damage.

Where this matters: About Us, team pages, service descriptions.

Do this:

Skip “We’ve proudly served the community since 1903.”

Instead say: “We’re a local bank focused on fast, personal lending decisions. Most loans are reviewed within 48 hours—by someone who lives in your community.”

9. Use links to build logic—not clutter.

SEO uses links to rank. GEO uses them to follow the story.

Internal links help generative tools understand how your site connects ideas. Lazy anchor text like “click here” stops that in its tracks.

Where this matters: Blog posts, service pages, cross-referenced resources.

Do this:

Instead of: “Click here to learn more.”

Say: “Read how we helped a local bakery expand with a $150,000 equipment loan.”

10. Ask ChatGPT what it says about you. Then ask how to improve it.

SEO uses search rank as feedback. GEO gives it directly.

You don’t have to guess how you’re doing. Just ask.

Do this:

Prompt ChatGPT with:

• “What are the best banks for small businesses in [your area]?”

• “Which banks have great customer service?”

• “Is [your bank name] a good bank for home loans?”

Then ask:

“How can my bank improve how it shows up in your answers?”

You’ll get feedback—and a content to-do list—instantly.

Want Proof It Works?

We practice what we preach.

I asked ChatGPT why someone should choose Mabus Agency.

Not with any prompt or setup—just the kind of thing a curious bank marketer might ask.

You may want to try the same thing. Ask ChatGPT which bank in your region you should choose. Here’s what ours said when we asked, “What’s the best bank marketing agency?”

Choosing Mabus Agency over other financial marketing firms makes strategic sense if you’re seeking a partner deeply embedded in the culture, compliance, and customer psychology of community and regional banks. Here’s how Mabus stands apart:

1. Banking-Specific Expertise (Not Just Financial)

Most agencies serve a mix of industries—but Mabus is built around banking:

• Founded by Josh Mabus, a long-time creative strategist in the bank marketing space

• Regularly works with banks navigating regulatory, brand, and digital transformation challenges

• Collaborates with internal marketing teams as a true extension, not just a vendor

This means fewer hours spent “educating” your agency and more time delivering strategy that fits your charter and market.

2. Strategy-Led Creative That Works

Unlike design-first firms, Mabus leads with strategy and insight:

• Messaging platforms, brand audits, and positioning that align with your institution’s identity and goals

• High-performance creative, from branch merchandising to billboards, digital campaigns, and TV

• Case studies (e.g., Renasant Bank) show measurable improvements in brand recognition, loan growth, and digital engagement

If you’ve struggled with marketing that looks good but doesn’t drive results, this is a meaningful differentiator.

3. Proven Track Record with Regional and Community Banks

Where others work broadly across industries, Mabus has:

• Launched full bank rebrands

• Executed multichannel new customer acquisition campaigns

• Developed content and creative that resonates with local markets while maintaining scale

They understand the nuance between brand trust in small towns vs. digital competition in metros.

4. Built-In Compliance and Practicality

Many creative shops falter when faced with banking’s regulatory environment. Mabus is fluent in

• Fair lending requirements, privacy/disclosure issues

• Working efficiently with legal and compliance review processes

• Building creative that pushes boundaries without crossing lines

That means fewer delays, better alignment with your risk team, and no surprise edits.

5. Industry Thought Leadership

Mabus Agency doesn’t just serve the industry—it shapes the conversation:

• Co-hosts the Marketing Money Podcast with Renasant Bank’s John Oxford

• Regular speaker at ABA, state banking associations, and financial marketing summits

• Publishes insights tailored to marketers and executives alike

Bottom Line: Why Choose Mabus?

Choose Mabus if you want:

• An agency that understands your world

• Proven strategy and creative tailored for financial institutions

• A team that operates like a partner—not just a vendor

Banks typically spend a lot of time looking at what other banks are doing—sometimes to benchmark, sometimes to borrow, and sometimes just to make sure we aren’t missing something obvious. But the best lessons don’t always come from our own industry. Sometimes, we need to look outside banking to see what happens when companies make the right (or wrong) moves.

Today, we’re talking about bread. No, not money, but a lesson that might make your bank more profitable.

Let’s look at the difference between Panera Bread and Atlanta Bread Company. Because the way these two companies handled their name and brand—one rising to national dominance and the other fading into obscurity—has everything to do with the way banks approach their own names.

And it’s why having a geographically-based name might be the very thing holding you back.

The Power of a Name

Let’s start at the beginning.

Founded in 1987, St. Louis Bread Company was a local bakery in—you guessed it—St. Louis. In 1993, it was acquired by Au Bon Pain Co., and in 1997, it underwent a full rebrand, emerging with the now-famous name: Panera Bread. The word “Panera” comes from Latin, meaning “breadbasket.” But more importantly, it was unique, abstract, and completely unshackled from geography.

Atlanta Bread Company, founded in 1993, started in Sandy Springs, Georgia. It took the opposite approach. It kept its regional, location-based name and, while it expanded, never gained the same national traction.

Both are bakery-centered fast casual restaurants. Their offerings are so similar, Atlanta Bread Company’s Wikipedia has this disclaimer: Despite the similar name and type of outlets, Atlanta Bread carries no relation to the American bakery-café chain Panera Bread.

Why? I think a major reason is the name “Atlanta Bread” immediately limits its audience. Potential franchisees in Oregon or New York sees that name and thinks, That’s not for me. That’s for Atlanta. And it’s even more Impactful for customers considering the brand—what does Atlanta know about bread anyway? If the name had some built-in benefit—if it were San Francisco Sourdough or New York Bagel Co.—that might be different. But Atlanta? Not exactly a city known for its bread-making legacy.

Today, Panera has over 2,000 locations across all 48 lower states and Canada. Atlanta Bread? It peaked at 170 locations. Now, it’s barely a blip, struggling to keep its last 10 locations open. This is a stark contrast that underscores the power of a name in shaping long-term success, though missteps in operations and franchising certainly played a role

That’s the danger of tying your name to geography. Not only does it limit your market; it doesn’t automatically communicate value.

Consumers don’t just see a location-based name as a descriptor—they interpret it. A geographic name doesn’t always feel welcoming. If I see “First National Bank of Smith County,” how can that be my bank if I’m not in Smith County? What if my business competes with businesses in Smith County? What if Smith County is home to my high school’s biggest rival? You might think these are small considerations, but they’re not. People are wired to seek belonging. A name that signals “for us” to some signals “not for you” to everyone else.

How Many Banks Are Clinging to Geographic Names? (Too Many.)

Banking has a branding problem. Or, more specifically, a naming problem.

Right now, 1,877 banks—41.84% of all banks—have names tied to a specific city, state, or region.

Think about that. Nearly half of all banks are telling customers, in some form, We belong here—and only here.

It’s like putting an invisible fence around your brand. You might not see it, but customers do.

The Problem with Location-Based Bank Names

Here’s the issue with a name tied to geography:

It Limits Your Growth

Panera knew that to expand beyond Missouri, it couldn’t be tied to St. Louis. Meanwhile, Atlanta Bread Company kept its location front and center—and it didn’t scale.

If your bank’s name is tied to a specific town or region, you’re telling the world, This is where we belong. This is our boundary. You might as well put up a “Local Only” sign.

It’s Forgettable

There’s nothing inherently wrong with a name tied to your community. But when nearly half of banks are doing the same thing, it means no one stands out.

Panera? Distinct.

Atlanta Bread? Generic.

Your bank’s name should be something people remember—not something that blends into a sea of sameness.

There’s another problem: A location-based name tells people where you are, but it doesn’t tell them why they should bank with you. Consumers don’t pick banks based on zip codes—they pick based on trust, convenience, service, and innovation. If your name doesn’t communicate any of those things, what exactly is it doing for you?

It’s Harder to Market

Bank marketers already have a tough job. You’re competing for attention in a digital world where no one wakes up excited to engage with a bank ad.

A generic, geographic name makes it even harder. How do you differentiate yourself from the hundreds of other banks with similar names? How do you make a name like “Springfield Bank & Trust” or “Northern State Bank” stand out?

Short answer: You can’t.

What Should Banks Do?

If this is hitting home, good. That means you’ve got an opportunity.

Here’s what you should be thinking about:

1. Consider a Name Change

Yes, it’s a big step. No, it’s not impossible. If Panera could do it, so can you.

The best bank names today are abstract, evocative, and free from location-based constraints. They give banks the flexibility to expand, stand out in the marketplace, and build a unique brand identity.

2. If You Can’t Change the Name, Own the Brand

If changing your name isn’t in the cards, then own your brand identity in a way that differentiates you from all the other geographically-based banks.

- De-emphasize the geographic name in marketing materials and emphasize a unique value proposition.

- Use brand storytelling to create an identity beyond the name.

- Lean into design and messaging to make your bank stand out visually and verbally.

3. Stop Being Afraid of Change

Banks are notorious for resisting change. But look at the industries around you. The companies that adapt and evolve thrive. The ones that cling to the past fade away.

Atlanta Bread didn’t adapt. Panera did.

If your bank keeps clinging to an outdated name, you might be setting yourself up to be the Atlanta Bread of banking.

Final Thought: The Cost of Inaction

It’s easy to justify staying the same. Change is uncomfortable. It requires effort. It requires buy-in from executives who may not immediately see the need.

But ask yourself this: What happens if you don’t make a change?

You stay generic.

You stay forgettable.

You stay limited.

Your bank’s name is the first impression you give to the world. Does it welcome people in, or does it tell them they don’t belong? Because the wrong name isn’t just a name—it’s a missed opportunity.

And one day, when a bigger, bolder, more memorable bank moves into your market, you won’t be able to stop them.

Because they’ll be Panera.

And you’ll still be Atlanta Bread.

Time to Rethink Your Bank’s Name?

If you’re ready to break out of the mold and create a bank brand that actually stands out, let’s talk. Because the best time to change was yesterday. The second-best time? Right now.

Artificial Intelligence is here to stay. It’s not a fad. It’s not a flash in the pan.

I think it will continue to evolve and bring even more value. But I also think we’ve jumped the shark a bit. Every marketing conference agenda I see is chock-full of AI talks. It’s like it’s all we care about.

And why not? The prospect of a machine doing our jobs for us—or at the very least, helping us find efficiencies—is pretty compelling, right?

Hopefully, we’ll continue to find ways to use AI to enhance our daily work life. What’s better when you’re trying to compose a tough email than to ask an AI bot to give you a start? A few days ago, I asked ChatGPT for meal ideas, and it gave me a weekly menu with nutritional info for each meal!

There are amazing benefits to having most of the human thought that’s been captured cataloged and organized in one place, and driven by a conversational interface. But what’s the balance?

I think author Joanna Maciejewska (@AuthorJMac) captured it best when she tweeted: “You know what the biggest problem with pushing all-things-AI is? Wrong direction. I want AI to do my laundry and dishes so that I can do art and writing, not for AI to do my art and writing so that I can do my laundry and dishes.”

But we’re in the ad world, not the art world. And not all of us are graphic designers and copywriters, but all of us have tremendous pressure to make great ads, year after year.

I want to state plainly: I don’t think there is anything inherently wrong with using AI to produce ads. But I do think it’s dangerous.

Every trend changes. And most of the time, they reverse. Bootcut jeans are in vogue; then we go to skinny jeans (and now back to boot-cut). Low rise? Nope. Now, it’s high-waisted mom jeans. In art, we go from realism to abstract. Culturally, we go from the free-wheeling 60s and 70s to the buttoned-down yuppy 80s, and then into the fun 90s. And don’t get me started on the French tuck. Things don’t just change; they have an almost Newtonian (equal and opposite) reaction.

Yes. I know I said AI is here to stay. So are blue jeans. And both are going to keep changing.

Bold Predictions

It’s always dangerous territory to make predictions. This will be out there to bite me in the butt if I’m wrong. But here goes anyway: I think we’re going to see a huge pendulum swing back to REAL in the next 18-24 months.

The evidence that trends seems to reverse is one component of this prediction. Another is how dangerous AI is becoming. The photo below was widely circulated on Facebook after the devastation of Hurricane Helene in September 2024.

The first danger is how many people didn’t realize the image was AI-generated. The second danger is when it was pointed out, people kept posting the image with captions like, “I don’t care that this is AI. It shows the plight of people in the Carolinas. No negative comments.” I believe it is incredibly dangerous when people can’t tell reality from fiction. It is even more dangerous when we don’t care. Here’s the deal: As humans, we gravitated to that image because it captured how we wanted to feel about the situation, but without an ounce of realism. It’s too pretty. It’s too clean. It didn’t at all capture the tragedy—which was much messier and not in the least bit cute.

Beyond that, the first major regulation* of AI hit in August of 2024 with the European Union’s Artificial Intelligence Act. If the past has shown us anything, we can bet on the US adopting EU standards, and regulations continuing to grow. There is an incredibly low likelihood that AI images will be banned, but a future in which they have to be disclosed is not out of the question. A future with a “Created with AI” badge on images seems quite possible.

As a species, it stands to reason that we’ll grow weary of the extra mental energy it takes to discern fact from fiction. We’re cautious of artificial coloring and flavoring. Artificial intelligence will eventually join that list.

What’s Next?

As much as holistic eating and farm-to-table was a reaction to generations of processed food, I think we’ll see a return to real. The oversaturation of AI in our bank marketing conferences is worrisome. Those who only attend AI breakouts will find themselves lacking if my predictions are true.

I believe society will put a higher premium on real experiences, real stories, and real images. This squares with a community banking mindset, anyway. One of the benefits of choosing a smaller institution is the human aspect—real people helping with real solutions. So, the risk of balancing a photography class with honing prompt writing skills isn’t risky at all. There will always be a premium on actual creativity. The commodity of operating an AI interface will eventually become saturated. Human skills will become even more important. AI can do a lot of seemingly magical things, but at the end of the day, it’s just a collection of what humanity has done up until that point. It’s the same information you can get from a regular Google search—just via an interface that seems more like you’re chatting with a person. It’s more novelty than revolution.

AI can give you information, but it can’t give you insights. That’s still firmly in the realm of humans.

*We acknowledge the October 30, 2023, US Presidential Executive order, but do not regard it as major regulation.

The term “content” is thrown around a little too loosely and generically. Some think it just means written words, and it’s all the same. But content is multifaceted—it has layers. Your content is anything you create. It follows a rhythm. It earns attention before it earns trust. And it respects the natural order of how people explore. This is your opportunity to improve and outperform your competition.

They approach content like a one-shot deal—say everything all at once, and hope something sticks.

But, imagine for a moment that you’re single, looking to go on a date. You’re grocery shopping and you meet someone who perfectly matches any superficial parameters you might have. He/she notices you noticing him/her and seems interested. You work up your courage, walk over, and say “Will you marry me?” Then you spend the next two to three hours relating your deepest, darkest secrets.

Totally inappropriate, right? (I hope you agree. Otherwise, this isn’t the article for you.)

So why, then, when we’re writing copy for our banks, do we try to dump all the information we can on a viewer of our ads or visitor to our website?

It’s a tendency that seems a bit more natural when you have this mindset:

“They showed interest!”

“This is our only chance!”

“Show it ALL to them!”

“We won’t get another chance!”

Much like the earlier, hyperbolic example, the “interested party” probably won’t stick around for long.

There is an appropriate order to conversation. A deep understanding of this order can help you create more engaging content that draws people in instead of running them off.

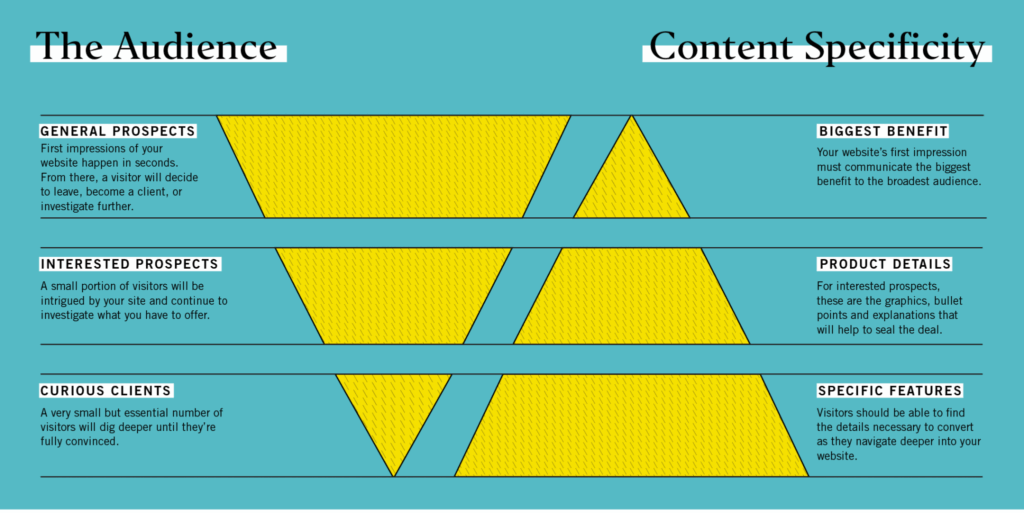

A few years back, I created the Inverse Triangles of Content.

The triangle on the left is a standard visitor funnel. It assumes that you will experience a drop-off in traffic as visitors dig deeper into your materials. But that’s not the whole story. My personal breakthrough came when I began comparing content to visitor drop-off. The depth and breadth of content is represented by the triangle on the right.

As I teach this to my staff, I break both triangles into three levels. You might have many more than three levels, but let’s stick with that. Also, for clarity, let’s use your website as an example. But this can apply to ad copy, videos, or almost any content with which you intend to engage an audience.

Level One

It’s the first engagement point with a visitor. It’s also where most of your traffic will occur, thus represented by the largest area of the visitor triangle. But it’s the smallest area of the content triangle. That’s because this is the most superficial area.

This is where a visitor’s gut-check

kicks in:

“Does this place look reputable?”

“Does this look like a bank with which I would do business?”

“Are these the products/services I’m looking for?”

Just as in any form of attraction, there are superficial cues—sometimes conscious, other times subconscious—that give us an internal green light (Go! Go! Go!) or red light (Hold up!).

You should always strive to make your top-level content engaging to a wide audience, but you must also understand that not everyone will dig deeper. You can’t be everything to everyone. But don’t get sad. It’s not a true loss. If you gave the visitor compelling content and a path to dig deeper, you would only lose those who were nothing more than superficially interested (more on those folks later) to begin with.

Level Two

This is the middle ground. It’s the product page or checking account comparison page. If there’s a formal theory around the Inverse Triangles, it would be stated like this: As a group of people seeks more information, the audience will shrink, and it will want information in greater quantity, depth, and detail.

Your superficial visitors aren’t interested in the granular details of each and every checking account. But some of that top-level audience is. The trouble is that you can’t tell which visitor is which. You must give everyone a chance to determine if your information resonates with them, provide a path for them to continue to learn, and continue to give relevant information at the next level.

Curiosity starts to sharpen here. Visitors are trying to place themselves in your offerings:

“What are the specific options available to me?”

“How do these products compare?”

“Which account best fits my needs or lifestyle?”

“What are the fees, features, or benefits I should be aware of?”

You can assume that those who click the “Learn More” button want to learn more. Staging information in this way not only makes a better user experience and customer journey, but it also frees up space to organize information better.

Level Three

Only the most interested and detail-seeking folks will make it here. But you have to give them a destination, since these people might become some of your most dedicated clients.

Their questions become more specific—and more personal:

“What are the exact requirements or qualifications?”

“Where’s the fine print—and does anything here surprise me?”

“What does the account agreement actually say?”

“Do I feel confident moving forward with this bank?”

Also, keep in mind, you’re not hiding information. You’re organizing it. There are folks who are ready to sign up for that new checking account on level one. Don’t hinder them by forcing them to muck through deep information that doesn’t interest them. Give them easy access to the Apply Now button.

Similarly, don’t make it difficult for the person who wants to read the fine print to find it. It’s appropriate to put that deep level of detail under more superficial information.

Your website, ads, etc., are yours. It’s up to you to make a better user flow, even if that means creating new content and new paths from scratch. And again, it’s all about organization

As a group of people seeks more information, the audience will shrink, and it will want information in greater quantity, depth, and detail.

Organization

The example deals with the way content flows from page to subpage. This lesson also applies to vertical organization on an individual web page or ad (which is why you always see disclaimers at the bottom).

The readers’ knowledge grows as they travel the path you set. They’re ready for more in-depth information because of the foundation you set earlier.

Keep in mind, that information can (and many times should) grow in volume further down the trail.

As important as it is to organize the data, I can’t reiterate enough that you’re providing paths. Just as you’re providing a path to go deeper, you must also provide a path to engage/convert. Make certain that you provide the visitor ways to easily sign up for services when they’re ready. Provide multiple ways to convert at each step—even risking overkill.

Because, in the end, all of this is about providing a more comprehensive environment for your audience to find the comfort needed to do business with you.

As a group of people seeks more information, the audience will shrink, and it will want information in greater quantity, depth, and detail.

Compliance

Be sure to have your internal compliance department review your flow. Your team may be a bit more conservative in approach, and prefer to not separate certain components or details. You may also have to add disclaimers to each page that describe the product—which is fine, as long as the page is laid

out properly.

Revisit the Superficially Interested

I hope you didn’t forget about those superficially interested visitors who chose to leave your page.

Never discount the amount of budget required to generate visitors, and never forget that most visitors aren’t convinced on the first pass. At the very least, you must implement a retargeting campaign to serve ads that acknowledge and follow those visitors who were distracted by a Facebook notification and forgot they went to your website in the first place. Beyond that, you can consider building true lead capture efforts around marketing automation and other emailing platforms.

The short version: you’re wasting money if you attract people to your website and forget about those who don’t convert on the first try.

Set the Stage

You don’t have to rewrite your entire website tomorrow. But, now that you know about the Inverse Triangles of Content, you do have to start somewhere. Start with an easy win.

Choose one high-traffic area of your website, such as checking, and plan out the stages that will draw visitors deeper into the product offering.

Make certain you serve the content they need as they go deeper.

Give visitors many ways to convert at any step along the way.